.png)

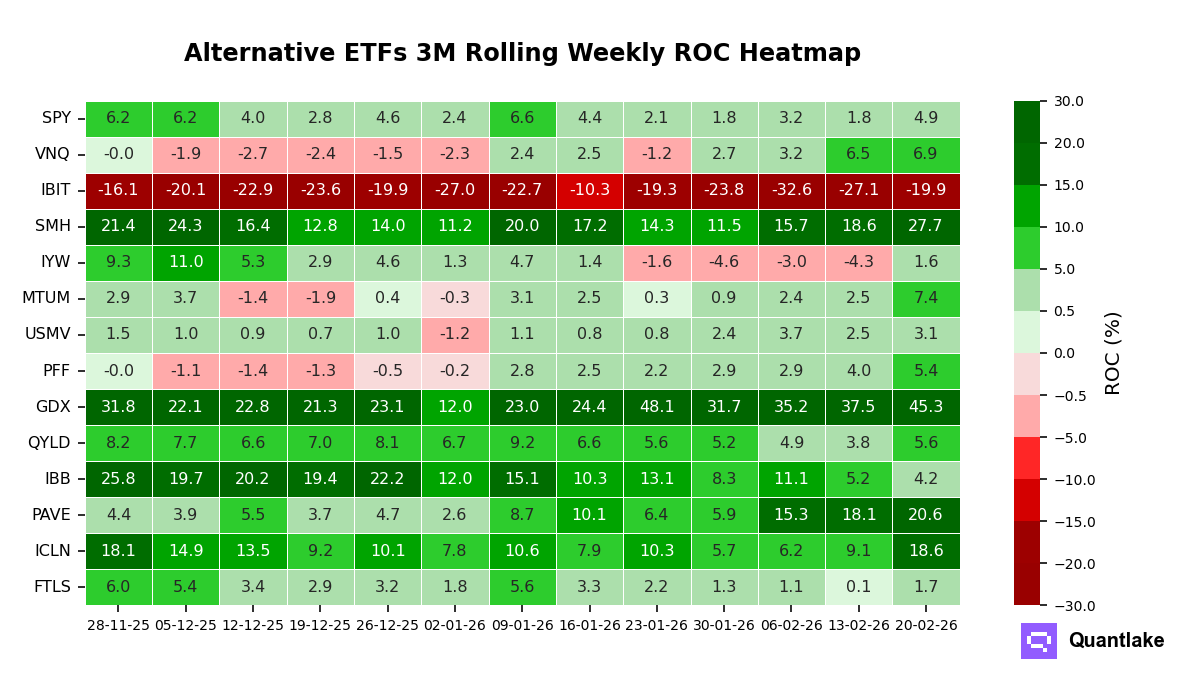

Alternatives broaden as clean energy and semis surge

Momentum across the alternative ETFs we track is now more unified, with leadership widening beyond the core real-asset complex. Versus last week’s narrower tape, this week showed a clearer, cross-theme acceleration, even as the laggard remained isolated.

The regime still reads as more than a simple equity-sensitive proxy. Global X U.S. Infrastructure Development’s correlation to the broad equity benchmark is 0.32 versus a 0.85 one-year average, alongside a 19.0-point alpha contribution, consistent with improved decoupling. VanEck Gold Miners also kept correlation moderate at 0.33 while carrying a 43.7-point alpha contribution.

Breadth strengthened to 13 of 14 ETFs showing week-over-week momentum improvement, and 13 remained positive on a 3-month trailing basis. The biggest accelerations came from iShares Global Clean Energy (+9.5 points), VanEck Semiconductor (+9.1 points), and VanEck Gold Miners (+7.8 points). The weakest shifts were iShares Biotechnology (-1.0 points), iShares MSCI USA Min Vol Factor (+0.6 points), and Vanguard Real Estate (+0.4 points). iShares U.S. Technology flipped positive.

In level terms, Gold Miners and Semiconductor sit in the top decile, with Infrastructure in the upper third. iShares Bitcoin Trust remains in the bottom decile, while U.S. Technology still sits in the lower half despite the sign flip.

Statistical stretch remains contained, with no ETF beyond a two-standard-deviation extreme. Vanguard Real Estate stands out at a 1.82 z-score and sits 1.5 points below its 12-month peak, a setup that flags normalization risk even as momentum holds firm.

Attribution continues to split the universe between idiosyncratic leaders and equity-sensitive proxies. Gold Miners, Infrastructure, and Real Estate pair lower-than-usual correlation with meaningful alpha contribution, reinforcing a diversification-friendly profile. By contrast, Semiconductor and Nasdaq 100 covered calls carry higher correlation and look more like beta expressions, even with strong momentum.

Our take: last week’s real-asset leadership view still holds, but this week’s breadth and the clean-energy and semiconductor surge extend the regime from narrow leadership into a broader, more synchronized advance.

![Alternative ETFs 3M Rolling Weekly Correlation Heatmap [vs SPY]](https://cdn.prod.website-files.com/654bb12ba4f14cf6cef8fb8a/6999ce61520db9b0ccf3d211_HeatMap_ALTS_Tactical_21022026_corr.png)