.png)

Tactical Participation Holds as Leadership Narrows

SUMMARY

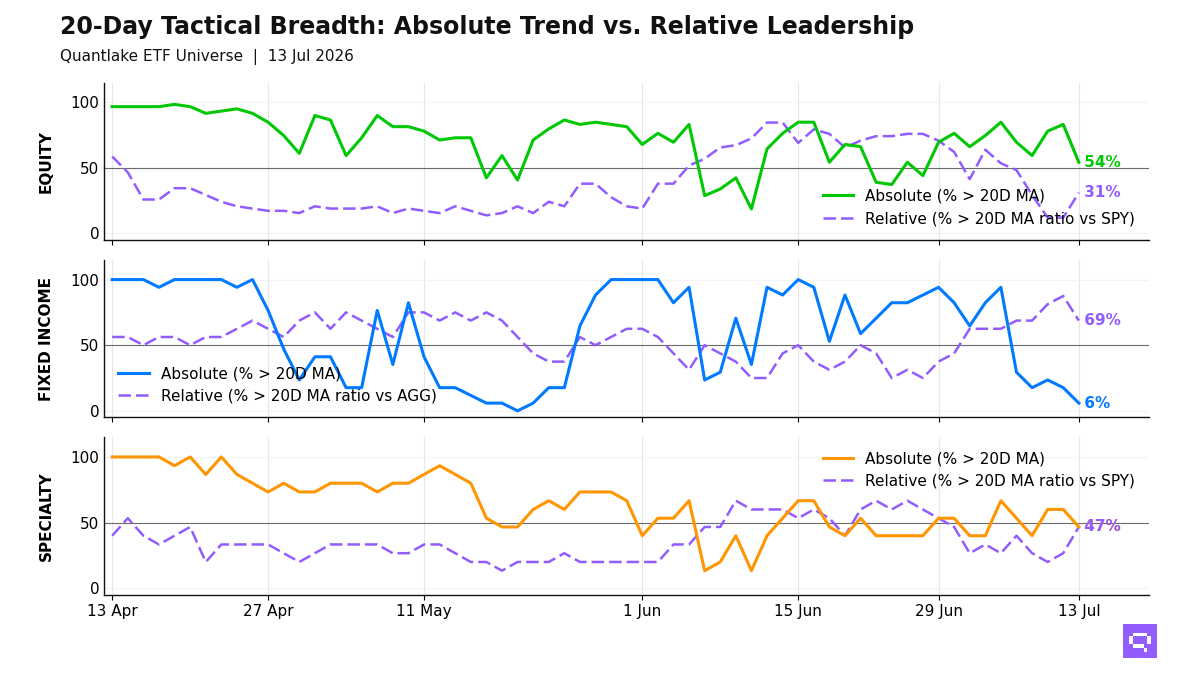

At Monday's close, we still saw powerful price participation across our ETF universe, but leadership narrowed further beneath the surface. In equity, 60 of 62 ETFs (97%, unchanged on the day) held above their 20-day moving average, while only 34 of 61 (56%, unchanged) outperformed their benchmark, leaving a +41pp gap as financials, US broad beta and ex-US equity led while low-volatility, China, Japan and India failed to confirm. Fixed income carried the same mixed structure: 17 of 17 ETFs (100%, unchanged on the day) stayed above their 20-day moving average, yet only 9 of 16 (56%, unchanged) led on a relative basis, with credit and EM debt ahead and Treasuries plus long duration lagging.

Alternatives were the clearest warning sign at the close: 12 of 13 ETFs (92%, +7.7pp) finished above their 20-day moving average even as relative breadth fell to 3 of 13 (23%, -30.8pp), a benchmark-led bucket with a +69pp gap as real estate, precious metals and diversified commodity exposures rose in price without keeping up. That deterioration in confirmation keeps our conviction measured across our coverage, because participation is high but genuine leadership remains concentrated.

20-Day Tactical Breadth

KEY TAKEAWAYS

- Financials XLF and US Broad Market VTI crossed above their 20-day relative averages, which fits the broader multi-horizon leadership already sitting in emerging markets, Developed ex-US equity, Taiwan, the UK, South Korea, Brazil, US cyclicals, momentum and value. By contrast, Japan EWJ crossed below its 20-day relative average despite a +2.0% 20-day return, so we read it as fading leadership rather than outright weakness, while Russell Growth IWF crossed up with a -0.5% 20-day return, which still looks like early stabilization; India INDA and Clean Energy ICLN remain on the weak side of that split.

- Across fixed income, daily, weekly and monthly relative strength stays concentrated in EM Debt (EMB), high-yield credit (HYG, JNK), Mortgage-Backed Securities (MBB), Preferred (PFF) and Investment Grade (VCIT), while International Aggregate (BNDX), government/treasury (IEF, IEI, VGIT) and long-duration (TLT) are the weak side of the tape. We see that as spread-product leadership over duration, so the lag is more about rate sensitivity than credit stress; short-duration exposure holding above its 20-day moving average without relative leadership fits the same stability-over-conviction message.

- Broad Commodities PDBC crossed above its 20-day moving average, but the alternatives bucket is not broadening in quality. Relative leadership is limited to copper and crypto-linked names, while Global REITs REET, Real Estate VNQ, Real Estate Sector XLRE and Silver SLV all crossed below their 20-day relative averages; SLV's -9.6% 20-day return makes that a clear deterioration inside a bucket dominated by price recovery without leadership.

FEATURED ETF — Highest 20-Day Relative Momentum Loss: SLV vs SPY

OTHER TECHNICAL SIGNAL EVENTS

──── EQUITY ──────

▲ Absolute Price Signals

Above 20D moving average:

iShares MSCI USA Min Vol Factor ETF USMV (20D perf: -1.24%)

Below 20D moving average:

Consumer Staples Select Sector XLP (20D perf: -3.22%)

⇄ Relative Strength Signals (vs SPY)

Above 20D moving average:

iShares Russell 1000 Growth ETF IWF (20D relative perf: -0.54%)

Vanguard Total Stock Market VTI (+0.28%)

Financial Select Sector XLF (+2.24%)

Below 20D moving average:

iShares MSCI Japan ETF EWJ (20D relative perf: +2.03%)

iShares Global Clean Energy ETF ICLN (-0.64%)

iShares MSCI India ETF INDA (-1.15%)

──── ALTERNATIVES ──────

▲ Absolute Price Signals

Above 20D moving average:

Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF PDBC (20D perf: +0.82%)

⇄ Relative Strength Signals (vs SPY)

Below 20D moving average:

iShares Global REIT ETF REET (20D relative perf: -0.79%)

SPDR Real Estate Select ETF XLRE (-1.32%)

Vanguard Real Estate ETF VNQ (-1.47%)

iShares Silver SLV (-9.57%)

Romain Gandon

CEO, Quantlake

Disclaimer: This report is for informational and educational purposes only and does not constitute investment advice.