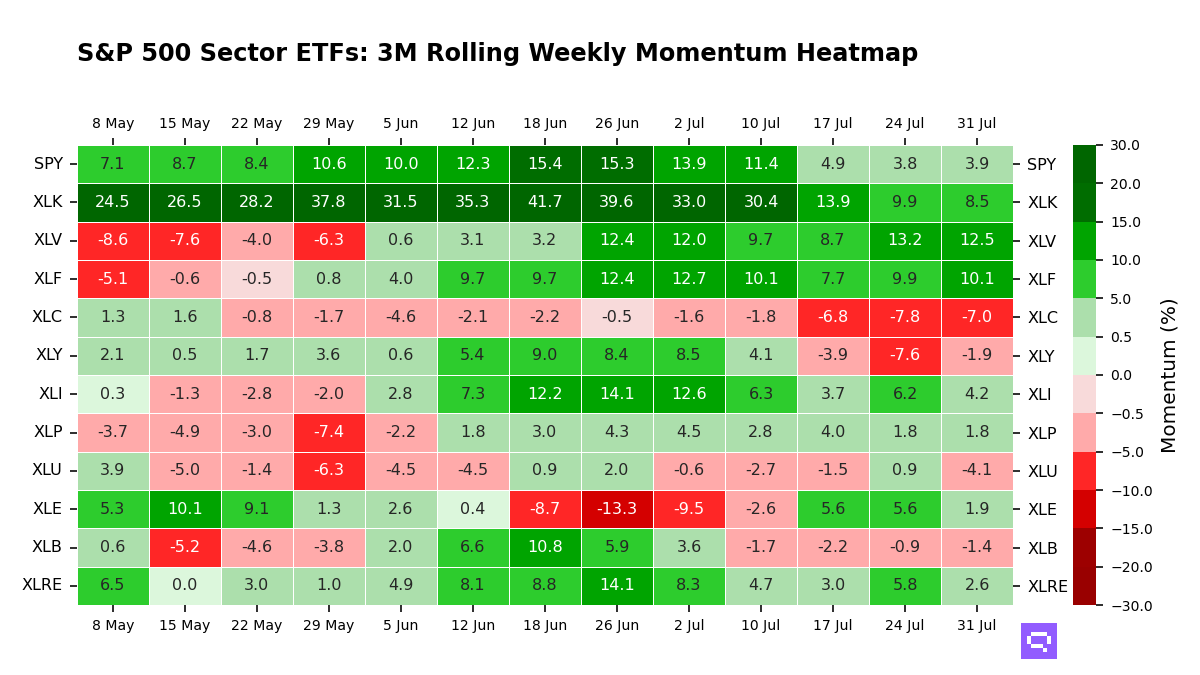

.png)

QHI Reading: Greed Lasts 36 Days as Momentum Cools

Greed Historically Trails Baseline Most in Three-Month Win Rate

Greed cooled over the week, and the Quantlake Herd Index (QHI) stands at 65.9 on July 31 after a 2.6-point daily rebound and a 7.1-point drop over the past five sessions. The index sits 3.5% below its 1-month average of 68.3 and 17.1% above its 12-month average of 56.3; it also set a new 1-week high. The 0.59 z-score places investor behavior above its long-run mean, so the current configuration is a cooling Greed regime with risk appetite elevated.

That gap appears in SPY's forward profile in the QHI sample since 2009: the 1-month hit rate is 63.5% against a 69.2% baseline, the mean return is 0.9% versus 1.2%, and the Sharpe is 0.82 against 1.07. The 1-month downside sits near baseline, with a 5th-percentile outcome of -6.0% and a worst-5% average of -8.7%, versus -6.1% and -9.6%; at three months the mean return is 1.7% against 3.6%, the Sharpe is 0.53 against 1.18, and the 5th-percentile and worst-5% outcomes reach -9.9% and -14.8%, versus -8.2% and -12.7%. The asymmetry sits first in weaker one-month participation and then in wider three-month downside tails, so the contrarian lean is mild at one month and broader by three months.

The Greed condition has held for 36 trading days, or 3.5 times its historical average. That tenure sits three days short of the 39-day maximum, which places the current run near the outer edge of prior Greed persistence. The 1-month standard deviation of 4.6 is 0.61 times its historical average, so optimism is cooling through compression and the regime is unusually durable.

Accessing Our Data

The full QHI historical series since September 1, 2009 is available via the Quantlake API for systematic integration. Learn more about the QHI methodology →

Data: 31 Jul 2026 · Daily Time Scale.

Romain Gandon

CEO, Quantlake

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Definitions

Quantlake Herd Index (QHI)

The Quantlake Herd Index (QHI) is a proprietary cross-asset behavioral sentiment composite ranging from 0 to 100 that measures extremes in investor psychology across the U.S. financial system.

It aggregates signals from U.S. equity momentum and breadth, equity market concentration dynamics, credit market risk appetite (high-yield vs investment-grade demand), implied volatility conditions, and credit spread behavior. These inputs are normalized into a single behavioral risk barometer reflecting the balance between risk-averse and risk-on investor behavior.

Because markets are influenced by behavioral biases, sentiment extremes frequently precede mean reversion in forward returns.

QHI Regimes

0–20: Extreme Fear

20–40: Fear

40–60: Neutral

60–80: Greed

80–100: Extreme Greed

Statistical Terms

Win Rate (Hit Ratio)

The percentage of historical periods in which SPY produced a positive return over the forward horizon. A win rate above 50% means positive outcomes historically dominated.

Median Return

The midpoint of the return distribution — 50% of outcomes fell above and 50% below this value. Less sensitive to extreme outliers than the average.

p25 / p75 (Expected Range)

The range within which the middle 50% of historical outcomes fell. p25 is the 25th percentile (bottom of the range); p75 is the 75th percentile (top). A tighter range indicates a more predictable regime; a wide range reflects high dispersion.

VaR 5% (Value at Risk)

The 5th-percentile return over the horizon — statistically, SPY has done worse than this figure only 5% of the time. A practical downside threshold: in 95 out of 100 historical observations, the actual outcome was better.

CVaR 5% (Conditional Value at Risk / Expected Shortfall)

The average of the worst 5% of historical outcomes. Where VaR 5% sets the threshold, CVaR 5% tells you what to expect on average when you are in that tail — a more complete picture of severe downside risk.

Full Range (min–max)

The absolute worst and best single-period outcomes recorded in the historical dataset. Useful as extreme-scenario context, but driven by one-off events (e.g. COVID crash, post-GFC recovery) rather than typical behaviour.

Sharpe Ratio

Annualised return divided by annualised volatility, measuring return per unit of risk. Higher values indicate better risk-adjusted performance in that regime.