.png)

Alt ETFs Cool Broadly as Real Assets Keep Lead

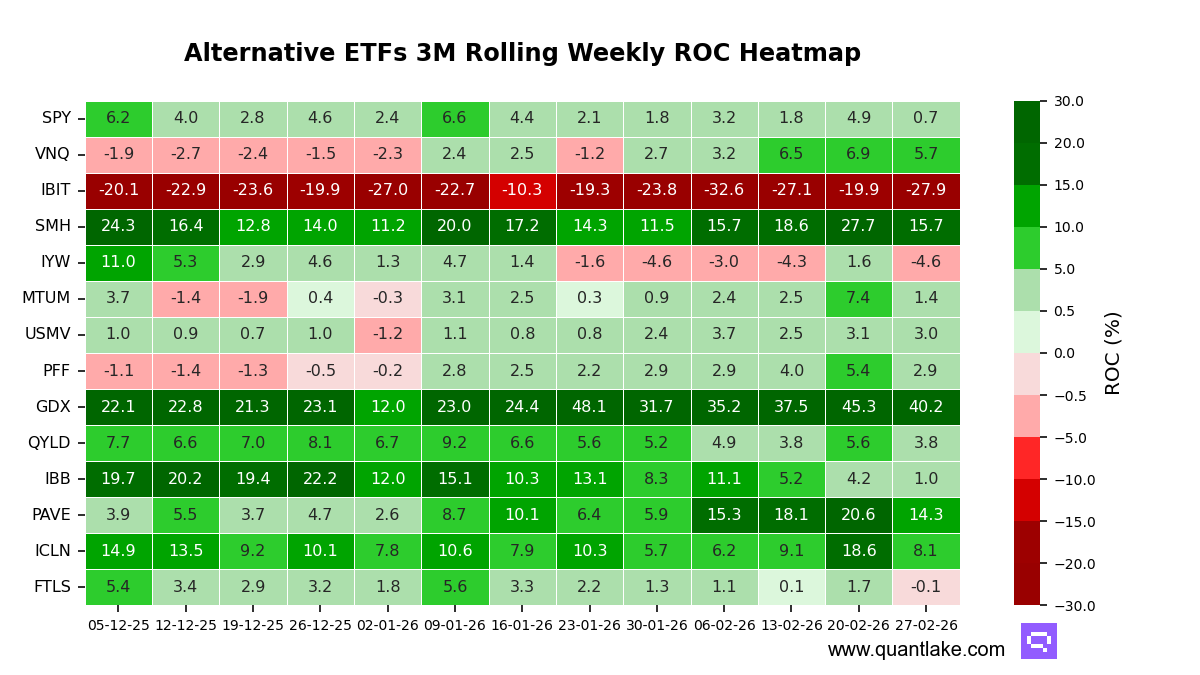

Momentum across the alternative ETFs we track is less synchronized than last week, as the earlier clean-energy and semis thrust gives way to a broad, uniform deceleration. Leadership remains anchored in real assets, but the tape is more dispersed as higher-volatility sleeves absorb the sharpest cooling.

Correlation and attribution still argue against a single beta tape. VanEck Gold Miners shows near-zero correlation to the broad equity benchmark at -0.02 and carries a 40.2-point alpha contribution. Global X U.S. Infrastructure Development also sits at low correlation, 0.11 versus a 0.84 one-year mean, alongside a 14.2-point alpha contribution, consistent with further decoupling.

Over the week, all 14 ETFs posted weaker 3-month trailing momentum versus the prior week, even as 11 of 14 remain positive in level terms. The smallest deteriorations were iShares MSCI USA Min Vol Factor (-0.1 points), Vanguard Real Estate (-1.2 points), and Global X NASDAQ 100 Covered Call (-1.8 points). The largest declines were VanEck Semiconductor (-12.0 points), iShares Global Clean Energy (-10.5 points), and iShares Bitcoin Trust (-8.0 points). iShares U.S. Technology and First Trust Long/Short Equity flipped negative.

Leadership in our universe remains concentrated at the top in Gold Miners and Semiconductor, with Infrastructure close behind in the upper tier. Clean Energy sits in the upper third despite the weekly cooling. Bitcoin remains in the bottom decile, while U.S. Technology and Long/Short Equity now sit in the lower half with negative momentum.

Statistical stretch remains contained across the complex, with no ETF beyond a two-standard-deviation extreme. Vanguard Real Estate sits 2.7 points below its 12-month peak with a 1.40 z-score, a setup that flags normalization risk rather than a clean extension. Bitcoin is 4.7 points above its 12-month trough with a -1.33 z-score, consistent with depressed but not capitulation-level positioning.

Attribution continues to split between idiosyncratic leaders and equity-sensitive proxies. Gold Miners and Infrastructure pair low correlation with large alpha contributions, keeping leadership primarily stock-specific within alternatives rather than benchmark-led. Semiconductor and Nasdaq 100 covered calls carry higher correlation and read more like beta proxies, even as their alpha contributions remain positive.

Our take: last week’s message of broadening leadership is challenged by this week’s unanimous momentum deceleration, even as real-asset leadership and idiosyncratic alpha remain intact at the top of the stack.

![Alternative ETFs 3M Rolling Weekly Correlation Heatmap [vs SPY]](https://cdn.prod.website-files.com/654bb12ba4f14cf6cef8fb8a/69a4462c95a92b1d401ea589_HeatMap_ALTS_Tactical_01032026_corr.png)