.png)

This Week in Quantlake ETFs: Style shifts to dividend and value

Dividend and value take control

Rotation stayed the defining feature in our equity ETF universe this week, with dividend and value exposures holding the leadership mantle while large-cap growth remains the key laggard. The tape looks broadly constructive, but differentiation persists between income and value on one side and growth on the other.

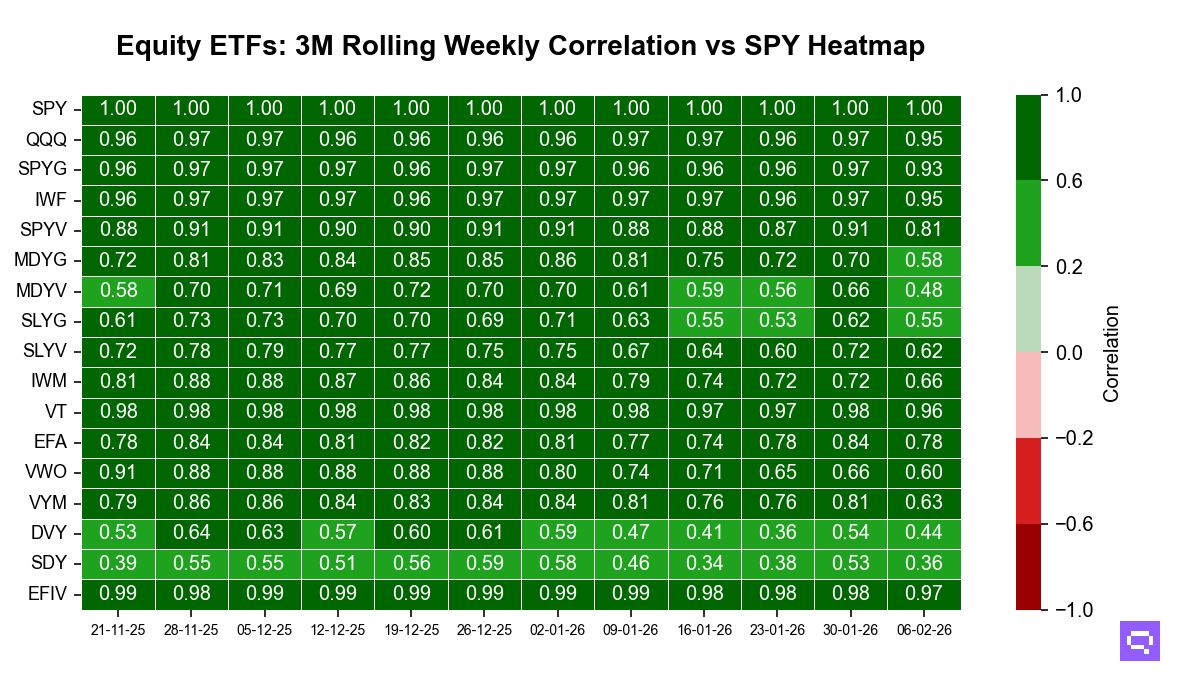

The regime holds because several leaders show materially lower correlation to SPY than their 1-year mean, alongside sizable positive alpha contribution. SPDR S&P Dividend ETF (SDY) shows correlation to SPY of 0.36 versus a 1-year mean of 0.68, while iShares Select Dividend ETF (DVY) sits at 0.44 versus 0.73, both consistent with improving diversification rather than pure beta participation.

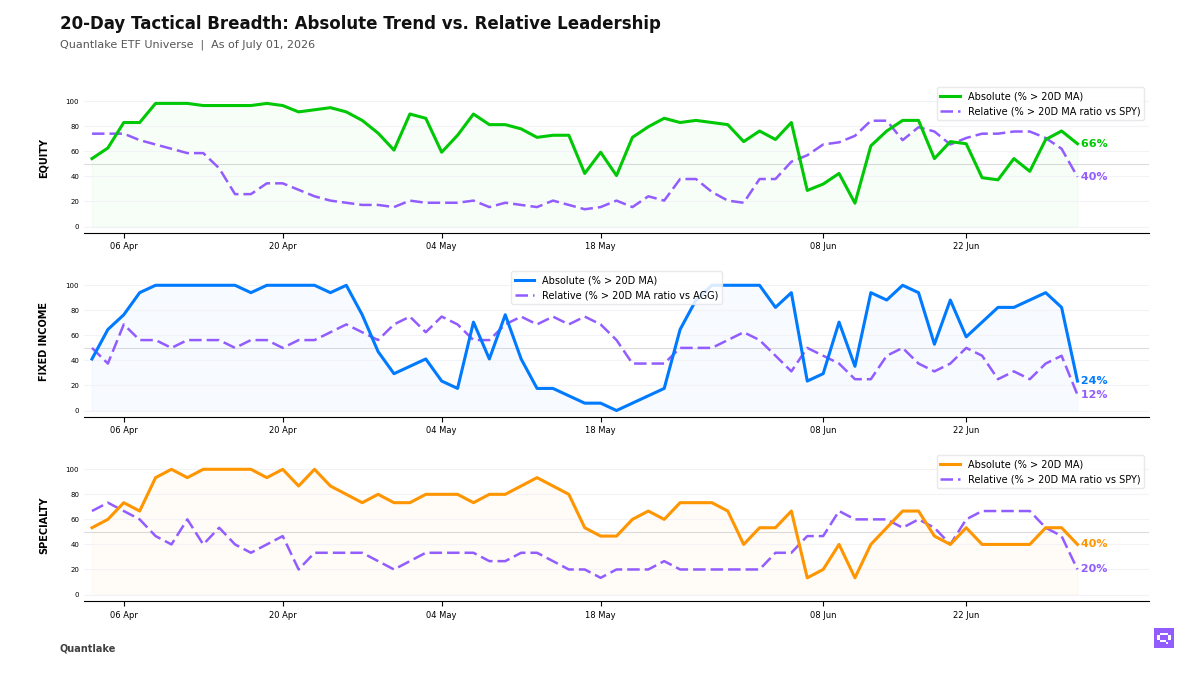

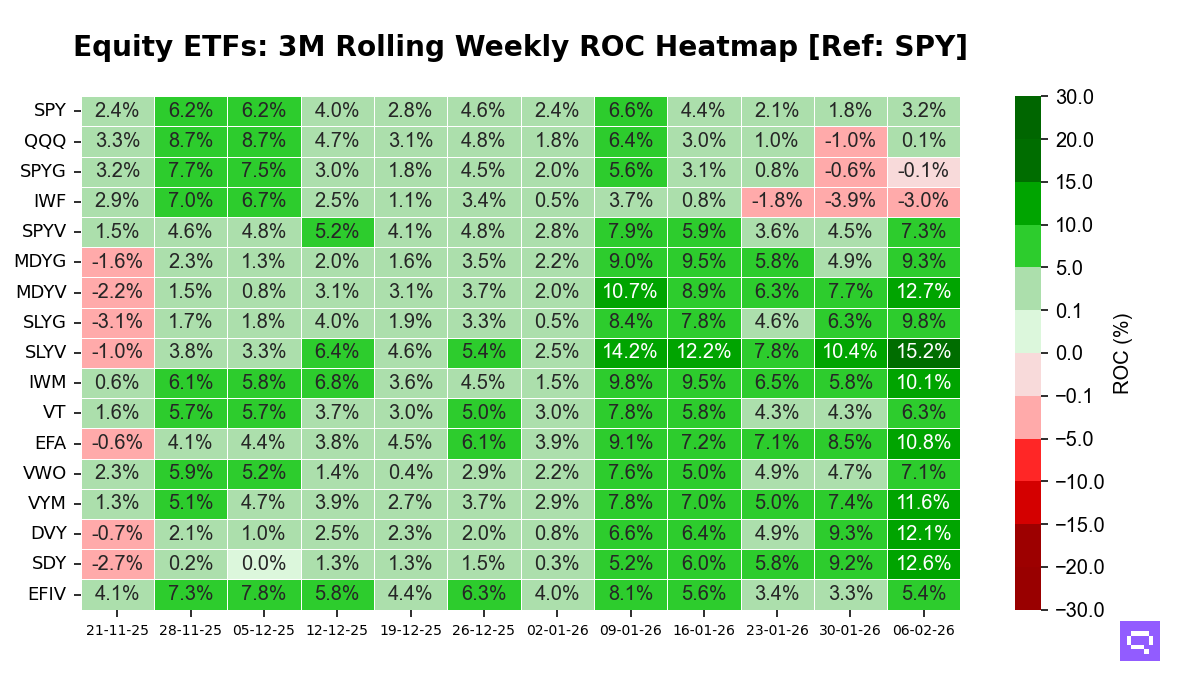

Breadth was unanimous over the week, with all 17 ETFs we track showing momentum improvement. The biggest week-over-week momentum gains came from SPDR Portfolio S&P 400 Mid Cap Value ETF (MDYV), up 5.0 points, SPDR Portfolio S&P 600 Small Cap Value ETF (SLYV), up 4.8 points, and SPDR Portfolio S&P 400 Mid Cap Growth ETF (MDYG), up 4.4 points. The smallest improvements were SPDR Portfolio S&P 500 Growth ETF (SPYG), up 0.5 points, iShares Russell 1000 Growth ETF (IWF), up 0.9 points, and Invesco QQQ Trust (QQQ), up 1.1 points. QQQ flipped positive.

In level terms, SLYV and MDYV sit in the top decile, with SDY and DVY close behind in the upper third. IWF and SPYG remain in the bottom decile, with QQQ still in the lower half despite the sign flip.

SDY is statistically stretched with a Z-score of 2.67 and sits at its 12-month peak, which raises exhaustion risk and a normalization risk. DVY is elevated but not extreme at 1.88 and remains near its 12-month peak.

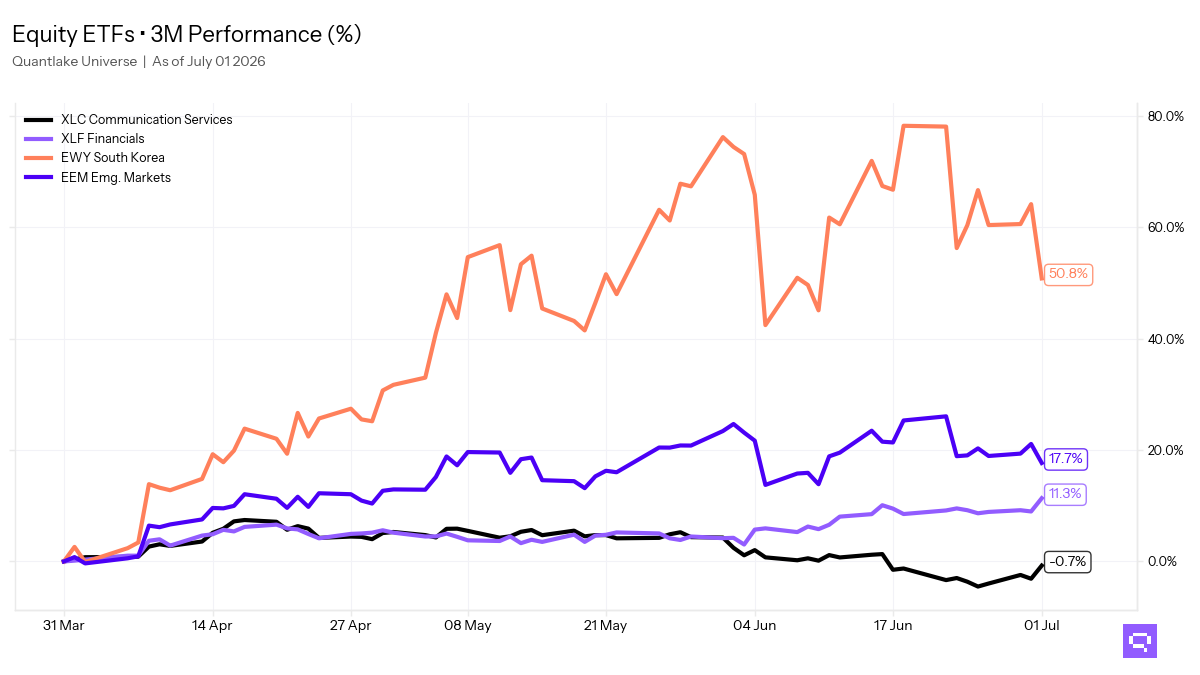

Leadership looks increasingly idiosyncratic: SDY, DVY, and MDYV pair lower correlation to SPY with large alpha contribution, pointing to dispersion rather than a single beta tape. By contrast, Vanguard Total World Stock ETF (VT) and iShares MSCI EFA Value ETF (EFIV) behave more like beta proxies, with correlation to SPY near 1.

Our take: the rotation toward dividend and value remains intact, and this week’s broad momentum lift did not change the core split between income-led strength and growth-led weakness. The key risk marker is SDY’s stretched positioning, while the rest of leadership looks elevated without the same statistical pressure.

Credit leads, duration still trails

Fixed income momentum is broad and increasingly balanced, with credit still setting the pace while duration remains the main drag. The curve profile looks flatter than last week, as core and intermediate exposures keep rebuilding traction even with the long end still lagging.

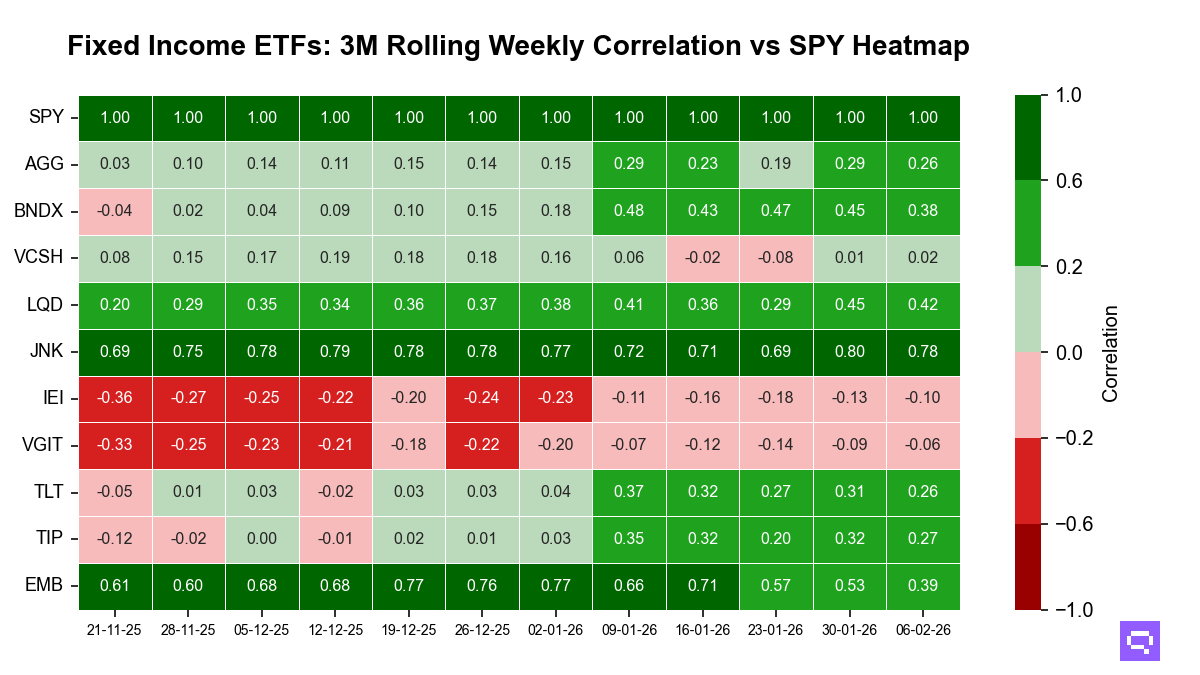

In linkage terms, the leadership mix is split between credit that behaves more like a risk-on proxy and rate exposures that retain more defensive characteristics. Correlation to the broad equity benchmark ranges from near zero in Vanguard Short-Term Corporate Bond ETF to strongly positive in SPDR Bloomberg High Yield Bond ETF, reinforcing a two-speed tape rather than a single unified trade.

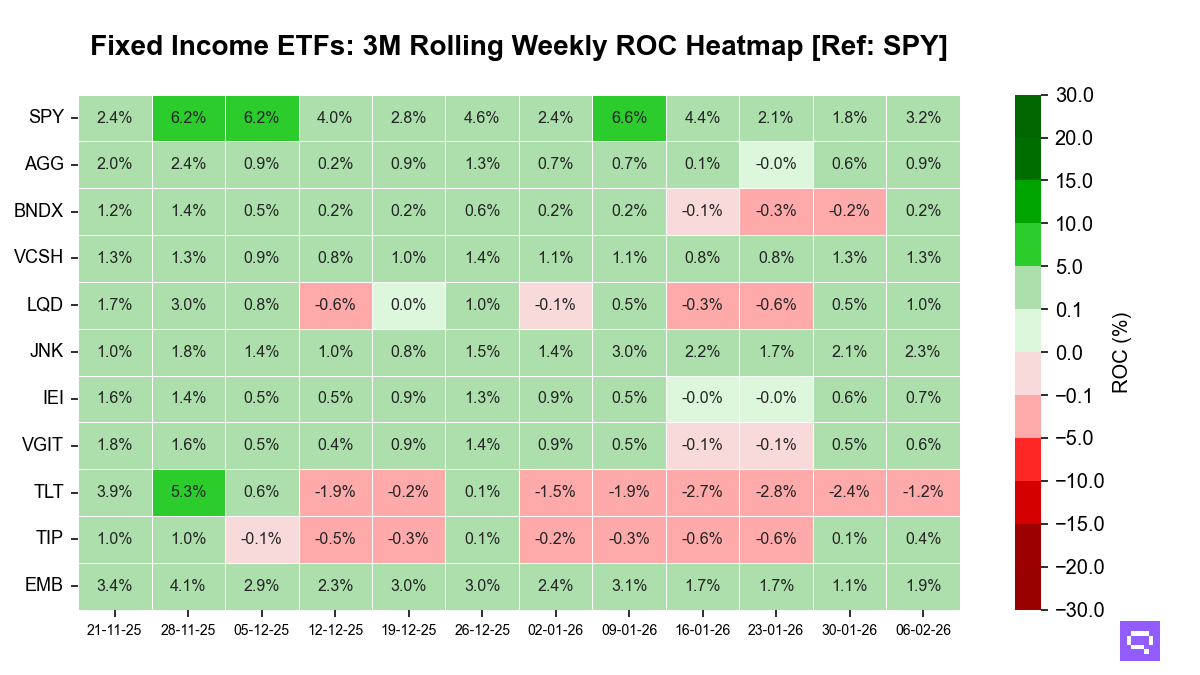

Over the week, every ETF we track strengthened on a 3-month trailing basis. The biggest momentum accelerations came from iShares 20+ Year Treasury Bond ETF at +1.2 points, iShares J.P. Morgan USD Emerging Markets Bond ETF at +0.8 points, and iShares iBoxx $ Investment Grade Corporate Bond ETF at +0.5 points. The smallest changes were Vanguard Short-Term Corporate Bond ETF at 0.0 points, iShares 3–7 Year Treasury Bond ETF at +0.1 points, and Vanguard Intermediate-Term Treasury ETF at +0.1 points. Vanguard Total International Bond ETF flipped positive.

In level terms, high yield and emerging markets debt sit in the top decile, with short-term corporates in the upper third. Core aggregate and investment grade are mid-pack, while the long bond remains in the bottom decile as the lone negative.

Statistically, nothing looks stretched: all Z-scores stay well inside typical ranges, with the most depressed readings still only around one standard deviation below their own means. Most funds also remain meaningfully below their 12-month momentum peaks, pointing to normalization rather than overheating.

Attribution underscores the split. High yield’s correlation to the broad equity benchmark is high at 0.78, so its leadership reads as beta-heavy, supporting upside participation but offering less hedging value in drawdowns. By contrast, short-term corporates show near-zero correlation at 0.02 with positive alpha contribution of +1.2 points, and emerging markets debt pairs moderate correlation of 0.39 with +0.7 points of alpha, signaling more internally driven leadership.

Our take: The regime is improving on breadth, but leadership quality differs by sleeve. Credit remains the momentum anchor, while core and intermediates are rebuilding without statistical excess. The long end is stabilizing on velocity, yet it still sits structurally behind the rest of the complex.

Happy Long-Term Investing!