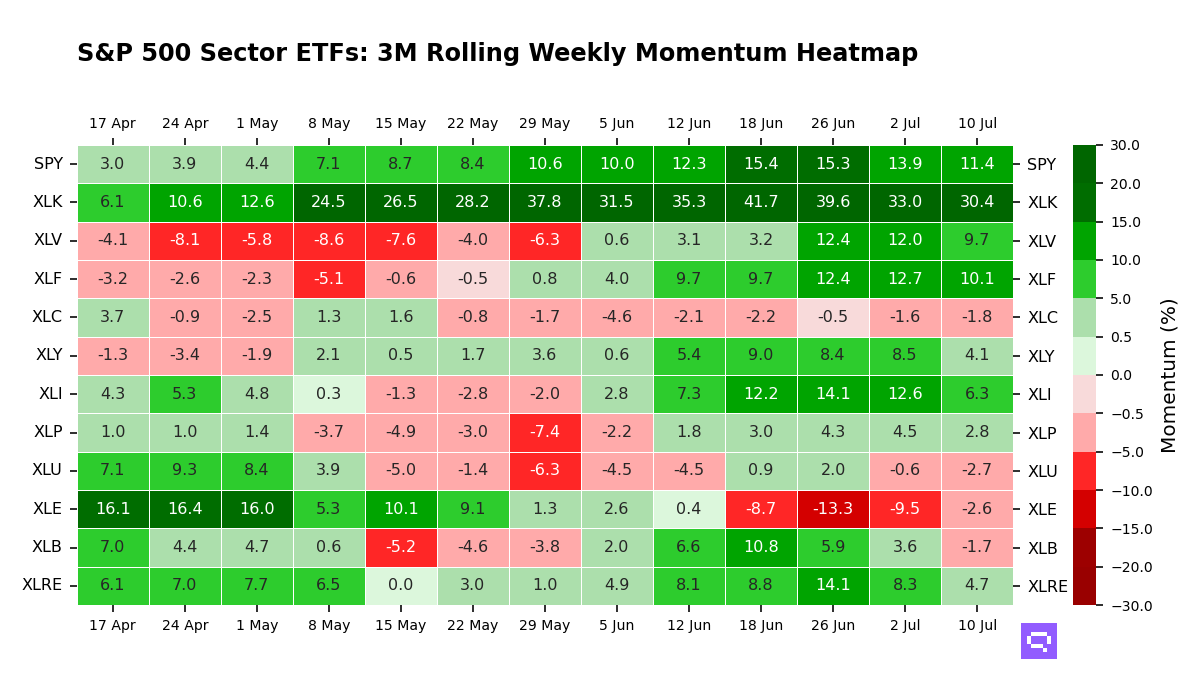

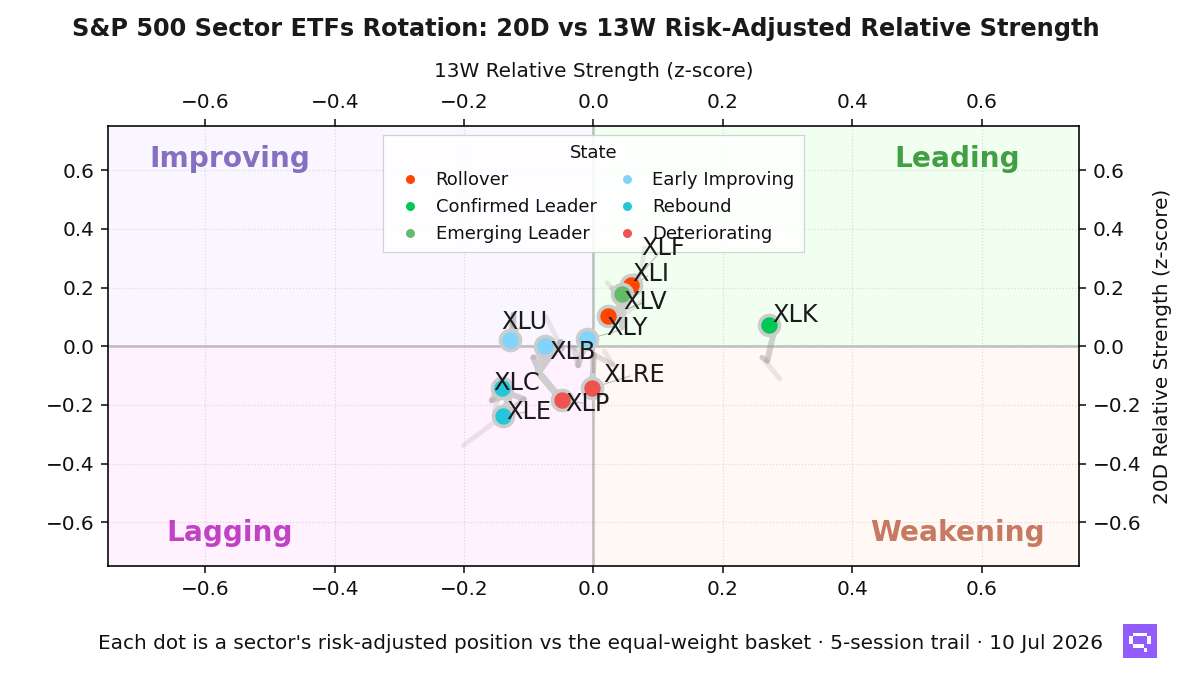

.png)

Tactical Trends: Fixed Income Rebounds as Relative Leadership Slips

Price breadth jumped, yet credit and munis carried the bond leadership

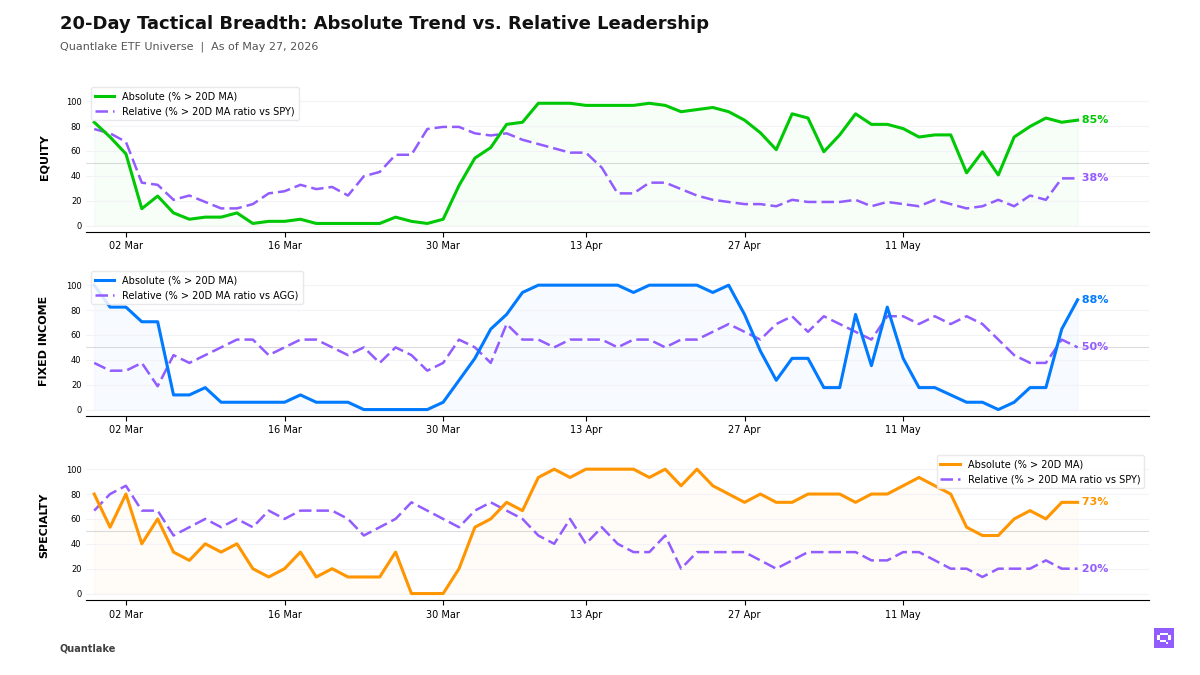

At the close, fixed income posted the clearest change in our ETF universe, with 15 of 17 ETFs (88%, +23.5pp on the day) above their 20-day moving average against 8 of 16 beating the Aggregate Bonds AGG (50%, -6.2pp). 7-10yr Treasuries IEF crossed above its 20-day moving average, and Muni Bonds MUB crossed above its 20-day ratio moving average versus AGG, but relative leadership stayed with credit, munis, EM debt, and long duration rather than intermediate Treasuries, MBS, TIPS, or short duration. That +38pp abs/rel gap leaves bonds in a benchmark-led rebound rather than a uniform recovery across rate-sensitive exposure.

Across equities, 50 of 59 ETFs (85%, +1.7pp) held above their 20-day moving average, but only 22 of 58 beat the S&P 500 SPY (38%, unchanged), leaving a +47pp gap. Materials XLB and Consumer Staples XLP regained their 20-day moving averages as relative leadership stayed concentrated in US growth, small caps, Taiwan, South Korea, and emerging markets, while Financials XLF, Utilities XLU, dividend, low-volatility, developed ex-US, and China exposures lagged. That keeps the equity advance tied to a concentrated leadership cluster rather than broad confirmation.

Specialty produced no new confirmed crosses this session, yet 11 of 15 ETFs (73%, unchanged) stayed above their 20-day moving average while only 3 of 15 beat the S&P 500 SPY (20%, unchanged). Semiconductors, momentum, and clean energy carried the relative winners. Copper CPER crossed below its 20-day ratio moving average versus S&P 500 SPY despite a positive 20-day relative return of 0.70%. That leaves specialty and commodities in a selective participation regime rather than a broad alternative-asset expansion.

20-Day Tactical Breadth

Key Takeaways

• Across daily, weekly, and monthly windows, equity relative leadership stayed concentrated in US growth and size exposures, Taiwan equity, South Korea equity, and emerging markets. Low-volatility, dividend-oriented US equity, developed ex-US equity, China equity, India equity, and several defensive sectors stayed on the opposite side of that alignment. The setup indicates persistent concentration rather than expanding participation.

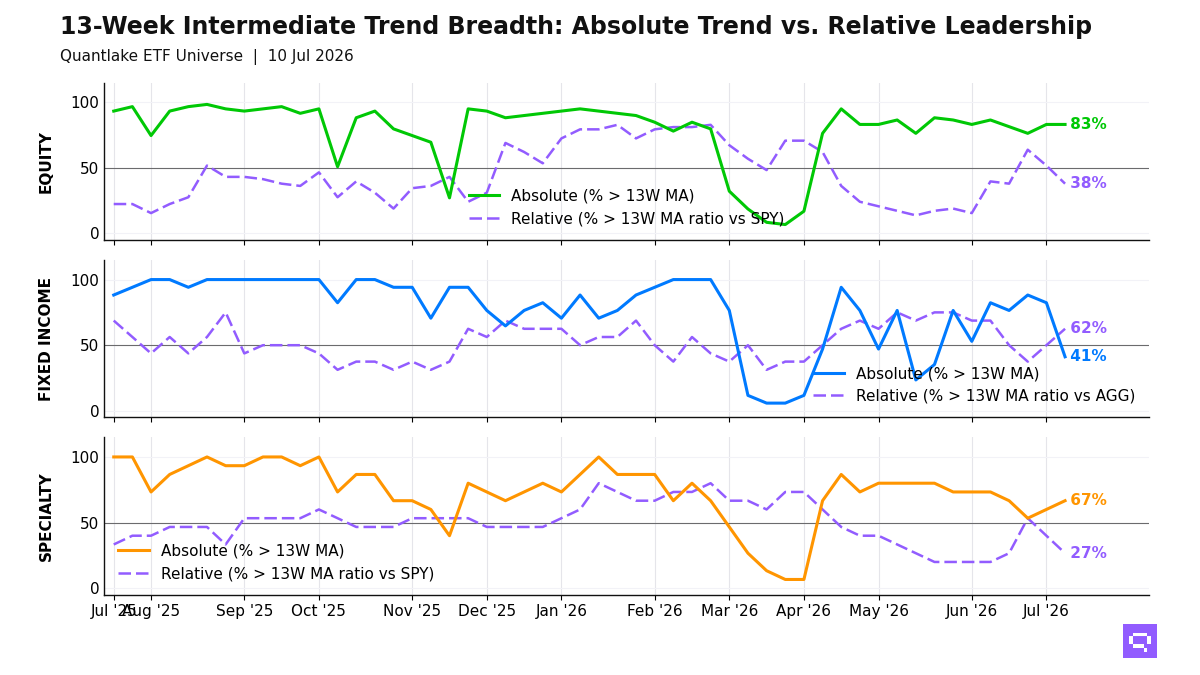

• Within fixed income, the relative rotation was not a simple duration bid. Long duration, investment grade, high yield, EM debt, international aggregate, and munis outperformed the Aggregate Bonds AGG, whereas 7-10yr Treasuries IEF, Int. Treasuries VGIT, Mortgage-Backed MBB, Short Corporate VCSH, and TIPS TIP lagged the benchmark despite several price cross-ups. The setup indicates broad price repair with leadership tilted away from intermediate government duration and short-rate stability.

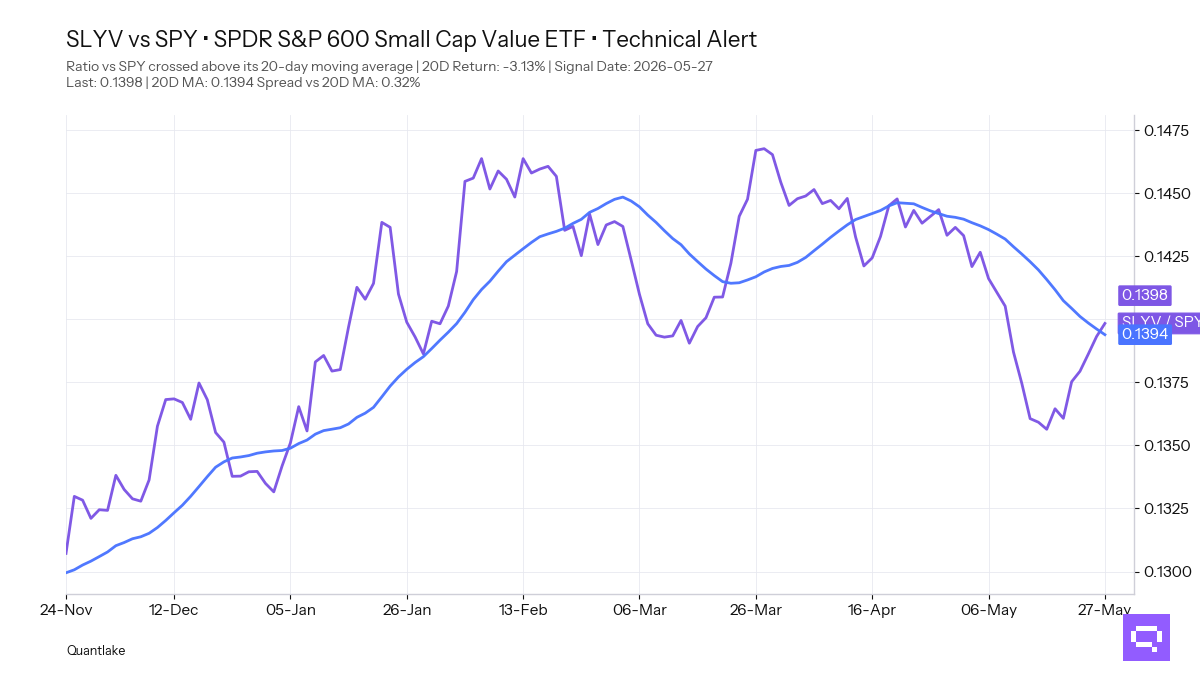

• Against the S&P 500 SPY, Value SLYV with a -3.13% period relative return versus SPY crossed above its 20-day ratio moving average. Small-Cap IJR and Consumer Discretionary XLY also crossed above their 20-day ratio moving averages versus the benchmark, yet all three still carried negative 20-day relative returns. The setup indicates early repair inside lagging equity cohorts rather than established leadership.

FEATURED ETF — SPDR® S&P 600 Small Cap Value ETF SLYV vs SPY

Other Technical Signal Events

EQUITY

↗ Price breakouts (cross-up 20D MA)

• JEPI - JPMorgan Equity Premium Income ETF · 20D perf: -0.72%

• XLB - Materials Select Sector · -0.43%

• XLP - Consumer Staples Select Sector · +1.81%

↘ Price breakdowns (cross-down 20D MA)

• XLF - Financial Select Sector · 20D perf: -0.83%

• XLU - Utilities Select Sector · -2.40%

↗ Leadership gains (cross-up 20D MA vs SPY)

• SLYV - SPDR® S&P 600 Small Cap Value ETF · 20D relative perf: -3.13%

• IJR - iShares Core S&P Small-Cap ETF · -2.49%

• XLY - Consumer Discretionary Select Sector · -1.49%

↘ Leadership losses (cross-down 20D MA vs SPY)

• EWJ - iShares MSCI Japan ETF · 20D relative perf: unch.

• MDYG - SPDR® S&P 400 Mid Cap Growth ETF · -0.17%

• SCHD - Schwab U.S. Dividend Equity ETF · -1.41%

FIXED INCOME

↗ Price breakouts (cross-up 20D MA)

• IEF - iShares 7-10 Year Treasury Bond ETF · 20D perf: -0.65%

• VGIT - Vanguard Intermediate-Term Treasury · -0.51%

• TIP - iShares TIPS Bond ETF · -0.26%

• PFF - iShares Preferred and Income Securities ETF · +0.77%

↘ Price breakdowns (cross-down 20D MA)

None on the close

↗ Leadership gains (cross-up 20D MA vs AGG)

• MUB - iShares National Muni Bond ETF · 20D relative perf: +0.16%

↘ Leadership losses (cross-down 20D MA vs AGG)

• VCSH - Vanguard Short-Term Corporate Bond · 20D relative perf: +0.27%

• MBB - iShares MBS ETF · -0.11%

SPECIALTY

No event on the close

COMMODITIES

↗ Price breakouts (cross-up 20D MA)

None on the close

↘ Price breakdowns (cross-down 20D MA)

None on the close

↗ Leadership gains (cross-up 20D MA vs SPY)

None on the close

↘ Leadership losses (cross-down 20D MA vs SPY)

• CPER - United States Copper LP · 20D relative perf: +0.70%

Romain Gandon

CEO, Quantlake

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results.