.png)

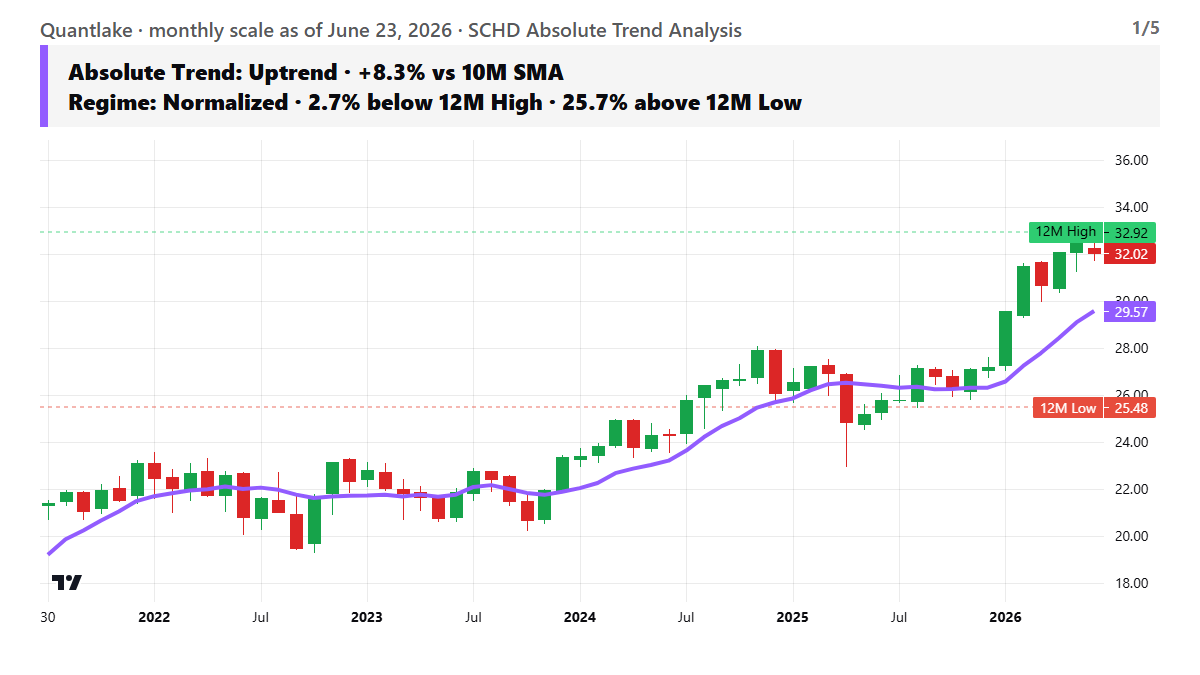

SCHD holds near its 12-month high above a rising SMA

Trend & Momentum

Schwab U.S. Dividend Equity ETF trades at $32.02, 8.3% above its 10-month SMA at $29.57; its SMA rose 6.4% over the past three months. Short-term pressure (1M -1.5%, 3M +4.4%) sits against firm medium-term action (6M +17.7%) and a 12M gain of +24.3%. Price crossed above its 10-month SMA in August 2025. SCHD moved up from an August 2025 low of $25.48 and reached its 12-month high of $32.91 this month; price closed 2.7% below that mark. 1Y realized volatility runs at 12.5%, against the 3Y average of 13.2% (z-score -0.7). The absolute trend is favorable.

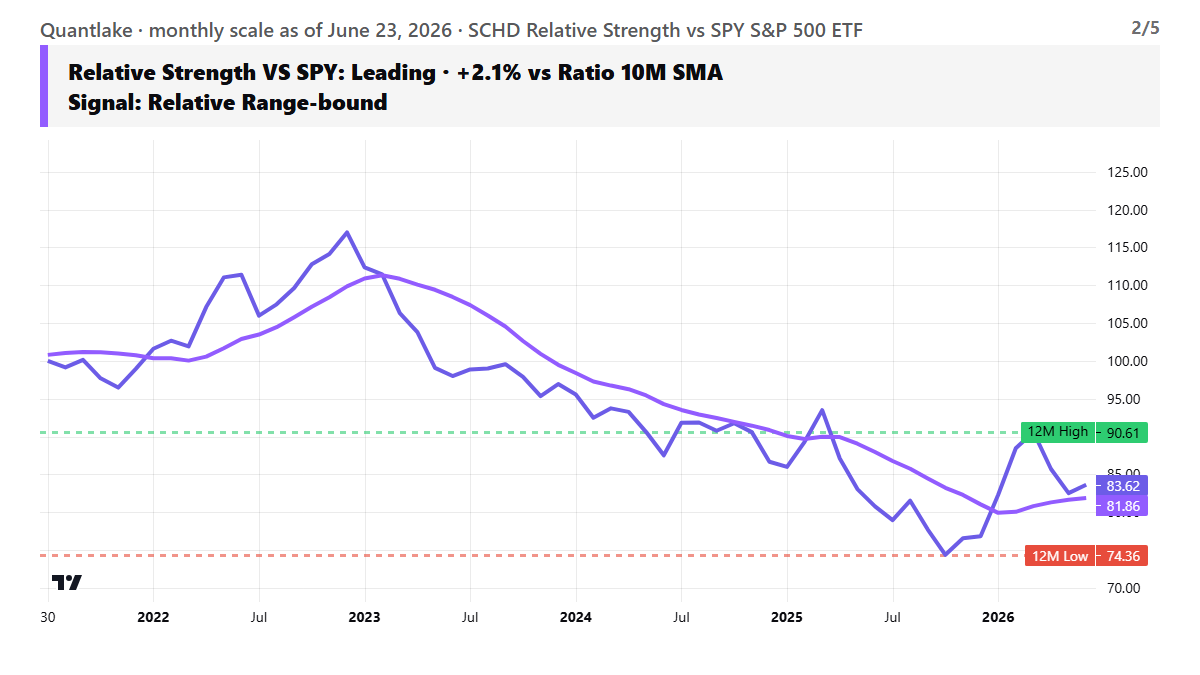

Relative Strength & Market Sensitivity

SCHD/SPY S&P 500, indexed to 100 at July 2021, trades 2.1% above its 10-month ratio SMA; its ratio SMA rose 1.3% over three months. Relative performance was uneven, with excess return at -7.7% over 3M and +3.5% over 12M. Market capture is asymmetric to the downside: 64.2% up / 80.2% down on 3Y, weakening to 56.5% / 83.0% on 5Y. 3Y up/down beta is 0.21 / 0.59; 5Y is 0.49 / 0.62. The asymmetric downside is more pronounced on 3Y than 5Y, a recent-regime feature (3Y gap -0.38, 5Y gap -0.13). After a 12M October 2025 low, the ratio last crossed above its 10-month SMA in January and then peaked at a 12M March high, 7.7% above the current level. Relative strength is not in a clean leadership regime.

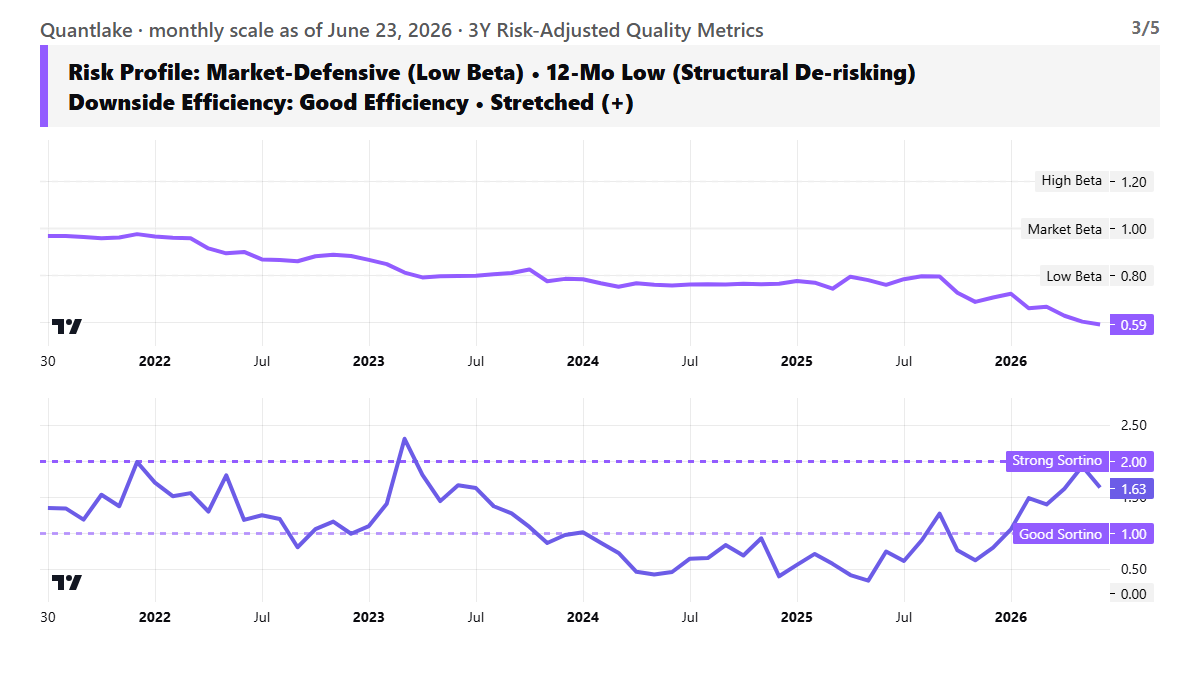

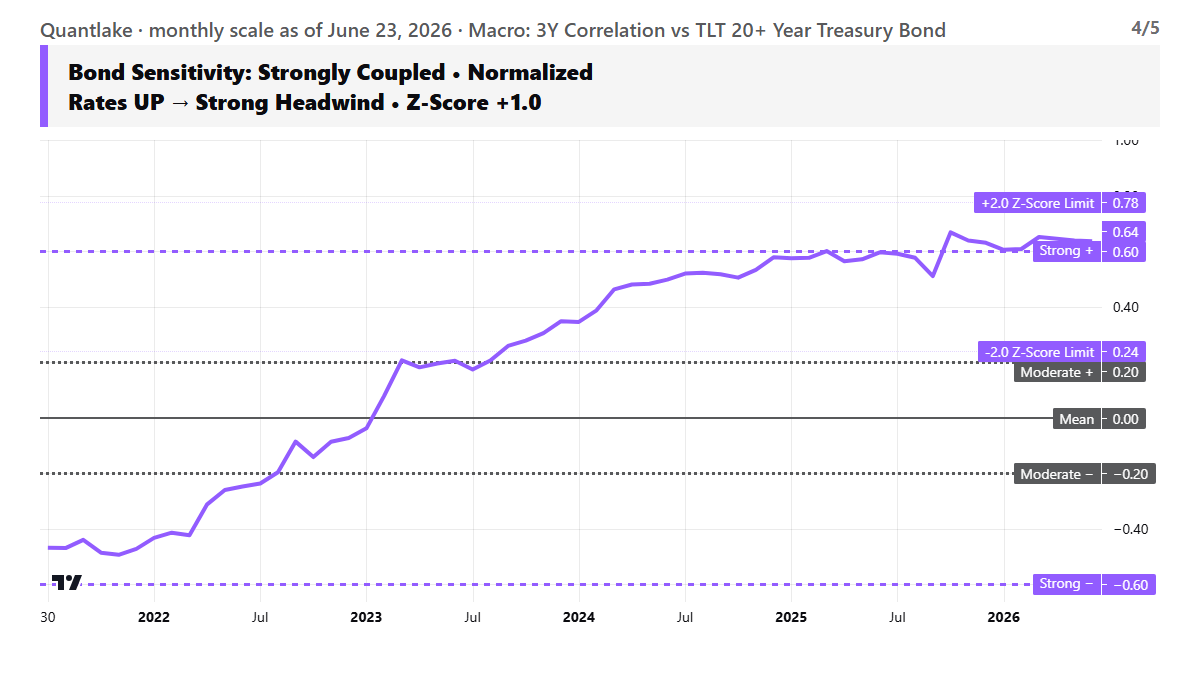

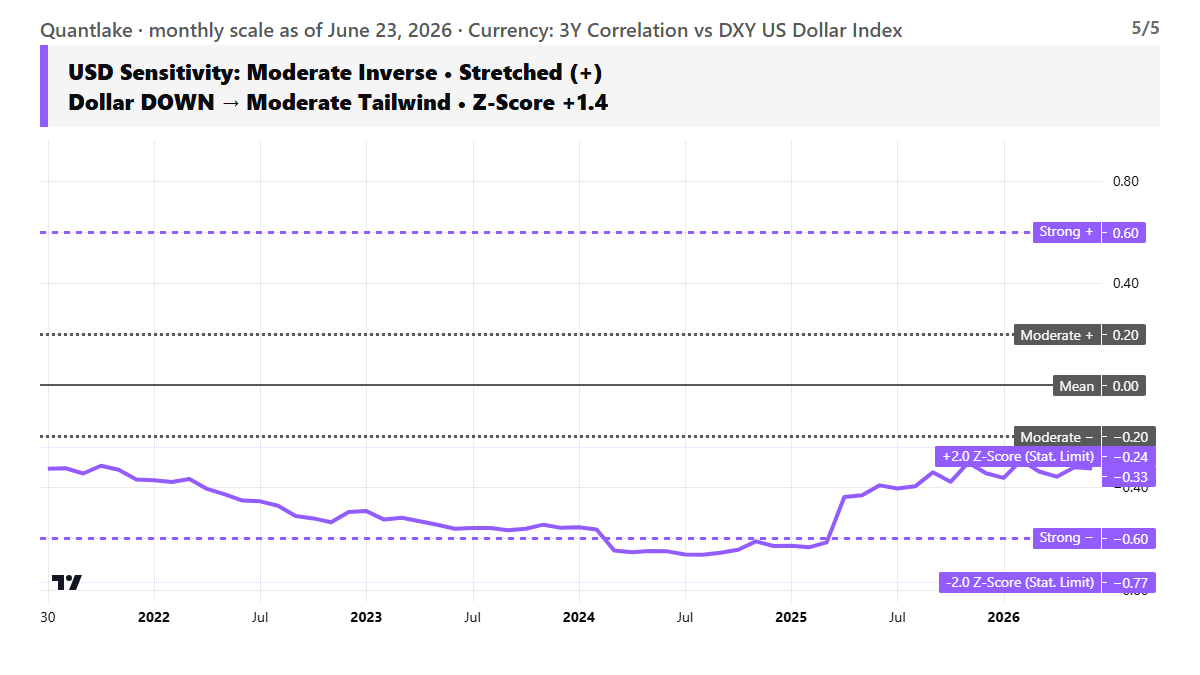

Risk & Macro Sensitivity

Return quality is strong on a recent basis, with 1Y Sortino at 5.6 against 3Y at 1.63. The 1Y reflects a concentrated recent spike; the 3Y is the more stable cycle reference. On the rate side, the fund's 0.64 3Y correlation to Long Treasuries TLT is strong, and with TLT 0.3% below its 10-month SMA, that leaves a limited headwind. On the dollar side, the fund's -0.33 3Y correlation to the US Dollar Index DXY is moderate, and with DXY 2.6% above its 10-month SMA, that creates a mild headwind. Risk structure is favorable on internal return quality, with rate direction through TLT the more material external constraint.

Romain Gandon

CEO, Quantlake

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Glossary

10-month moving average (SMA): A long-term trend filter popularized by Meb Faber's tactical asset allocation research. It averages the trailing 10 months of closing prices. Price above the line points to a structural uptrend; price below points to a downtrend.

SMA slope: The rate of change in the moving average line itself over a specific timeframe (such as three months). A flat slope confirms a trendless consolidation; a steepening slope confirms that trend momentum is accelerating.

Beta: A measure of an asset's co-movement with the S&P 500. A beta of 1.0 means the fund moves roughly in step with the market average; above 1.0 means it tends to swing harder than the market in both directions; below 1.0 means its swings are dampened. Beta measures market sensitivity, not the independent size of the fund's own price swings (which is volatility).

Upside / Downside beta: The standard beta calculation split into two environments: months when the S&P 500 is up vs. months when it is down. Upside beta shows how much a fund participates in market rallies; downside beta shows how much it gives back during market drawdowns.

Asymmetric upside / downside: The variance between upside and downside beta. 'Asymmetric upside' is an offensive profile where a fund captures more of the market's gains than its losses. 'Asymmetric downside' is a defensive vulnerability where a fund participates more fully in market declines than in recoveries.

Up-capture / Down-capture: The fund's average monthly return during S&P 500 positive months expressed as a percentage of the market's return (up-capture), and the same calculation for negative months (down-capture). Example: A fund with 114% up-capture and 52% down-capture rises 14% more than the market in up-months on average, and falls only about half as much during down-months.

Excess return: The fund's net return minus the S&P 500's return over an identical timeframe. This is cumulative over each specific window (1M, 3M, 6M, 12M) and is not annualized. It serves as the baseline measure for relative strength.

Indexed to 100: A method of rebasing the fund-to-S&P 500 ratio to a fixed reference date (such as June 2021 = 100) to make relative changes easier to read. Today's value reads directly as the cumulative percentage change in relative strength since that anchor. A reading of 115 means the fund has beaten the market by 15% since the starting date.

5-year percentile: The statistical ranking of the current data point within the asset's own rolling 5-year history. The 100th percentile represents a historical high for the range; the 50th percentile marks the exact historical median; the 1st percentile sits at the absolute floor.

Realized volatility: The standard deviation of a fund's actual monthly returns over a trailing 1-year window, multiplied by the square root of 12 to express it as an annual figure for easier comparison. Higher percentages imply wider price swings.

Sortino ratio (Downside efficiency): A risk-adjusted performance measure that only penalizes negative swings (losses) rather than general volatility. It measures the excess return earned per unit of downside risk. As a rough guide, readings above 1.0 are solid and above 2.0 are strong, though thresholds vary by asset class. Short-term (1-year) windows can be inflated by recent, low-volatility momentum bursts; the 3-year rolling window serves as the more reliable full-cycle benchmark.

Z-score: A statistical measure showing how far a current price or ratio sits from its own 3-year rolling average, measured in standard deviation units. Readings beyond +/-2 are statistically unusual; whether the data point reverts to the mean or continues to stretch depends on whether the prevailing trend is intact or weakening.

Correlation: A mathematical value from -1.0 to +1.0 measuring the consistency and direction of co-movement between two assets. +1 means they move in lockstep; -1 means they move in opposite directions; 0 means no consistent relationship. Correlation describes the direction and consistency of the move, not the absolute size of the price impact.

Headwind / Tailwind: An assessment of whether the macro environment is currently working for or against a fund. It is built from two distinct inputs: (1) how the fund correlates with a macro asset like Treasuries (TLT) or the US Dollar (DXY), and (2) whether that macro asset is itself in an absolute uptrend or downtrend. A fund positively correlated with bonds gets a tailwind when bonds are rising and a headwind when bonds are falling. A fund negatively correlated experiences the exact inverse.

Relative drift: The annualized rate of change in the ratio between the fund and the S&P 500 benchmark. It tracks the clean acceleration or deceleration of relative strength over time, independent of short-term price noise.

Lookback window: The specific historical timeframe used to calculate a metric (such as 1-year, 3-year, or 5-year windows). Shorter windows are highly sensitive to recent momentum shifts; longer windows smooth out noise but blend together multiple market environments.