.png)

Navigating New ETF Frontiers: Rotate as breadth narrows

Real assets hold the lead as leadership narrows

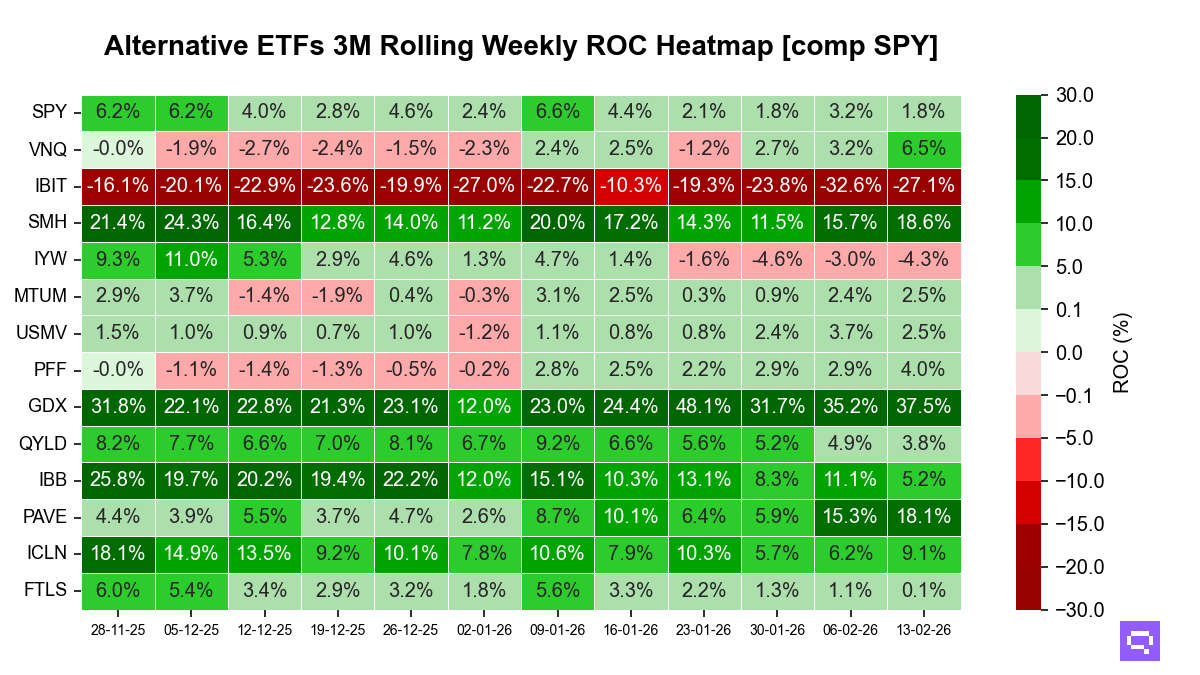

Alternatives momentum across the ETFs we track stayed tilted toward real assets, with gold miners and infrastructure still setting the pace while crypto-linked exposure remained the clear laggard. Compared with last week, the tape looked less uniformly constructive as fewer constituents improved on the week and the leadership gap widened.

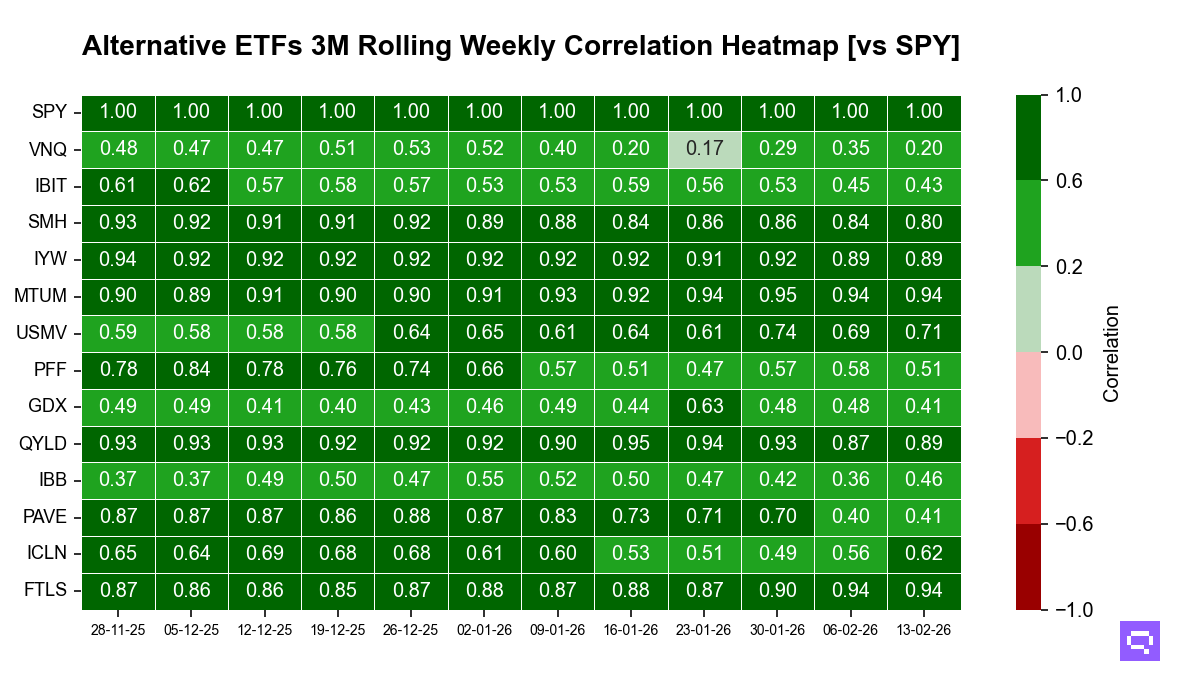

That dispersion still validated as more than simple equity sensitivity. Global X U.S. Infrastructure Development carried a 0.41 correlation to the broad equity benchmark, far below its 0.86 one-year average, alongside a 17.4-point alpha contribution. VanEck Gold Miners also sat at a 0.41 correlation versus a 0.25 average, while keeping alpha contribution elevated at 36.8 points.

This week, breadth cooled to 8 of 14 ETFs showing momentum improvement, while 12 remained positive on a 3-month trailing basis. The biggest week-over-week momentum accelerations came from iShares Bitcoin Trust, up 5.5 points, Vanguard Real Estate, up 3.3 points, and VanEck Semiconductor, up 2.9 points. The sharpest decelerations were led by iShares Biotechnology, down 5.9 points, iShares U.S. Technology, down 1.3 points, and iShares MSCI USA Min Vol Factor, down 1.2 points. No ETFs flipped positive or flipped negative.

In level terms, Gold Miners and Semiconductor sit in the top decile of our cross-section, with Infrastructure in the upper third. Bitcoin Trust remains in the bottom decile, alongside U.S. Technology.

Statistical stretch stayed contained. Vanguard Real Estate stood out with a 1.78 z-score and sat just 1.9 points below its 12-month peak, a setup that raises normalization risk even as momentum remains firm.

From an attribution lens, Gold Miners and Infrastructure continued to look alpha-led within alternatives, pairing moderate benchmark linkage with outsized idiosyncratic contribution. Semiconductor and Nasdaq 100 covered calls behaved more like equity-sensitive proxies, with correlations near the high end of our universe and smaller alpha shares. Real Estate’s correlation remained well below its own history, consistent with improved diversification while momentum holds positive.

Our take: last week’s real-asset leadership call still holds, but this week’s data underscored a more uneven tape, with widening separation between alpha-led winners and equity-linked proxies even as crypto stabilized off the lows.