.png)

Dividend ETFs Lead as Equity & Bonds Cool in Unison

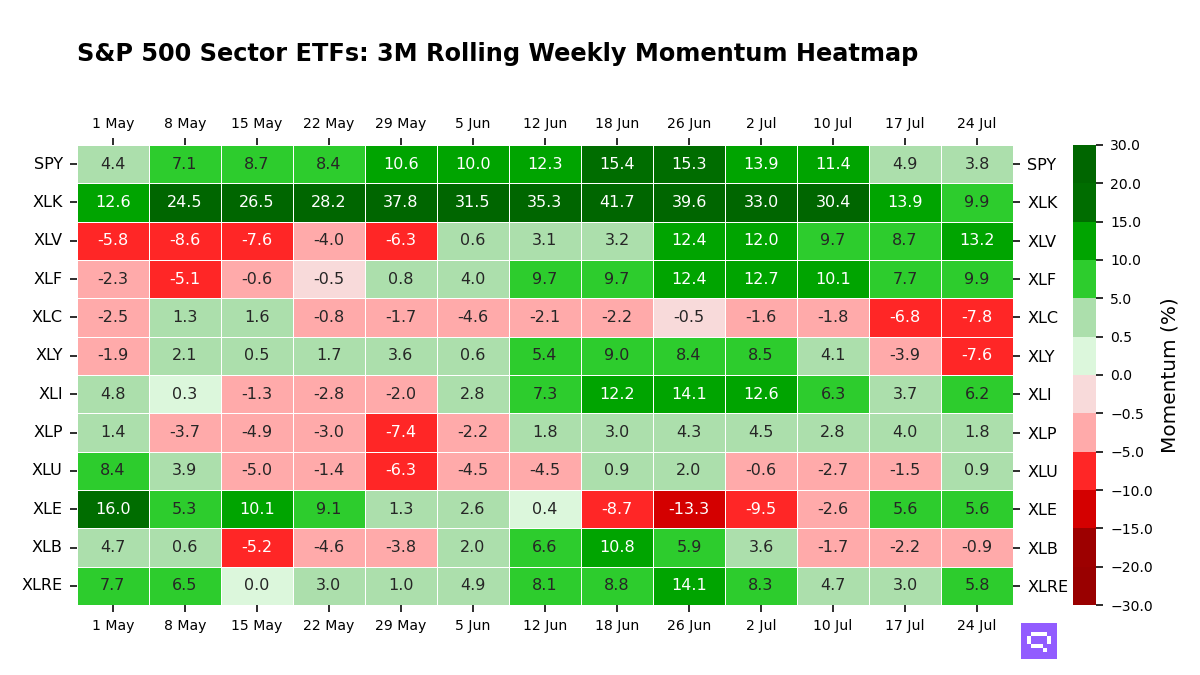

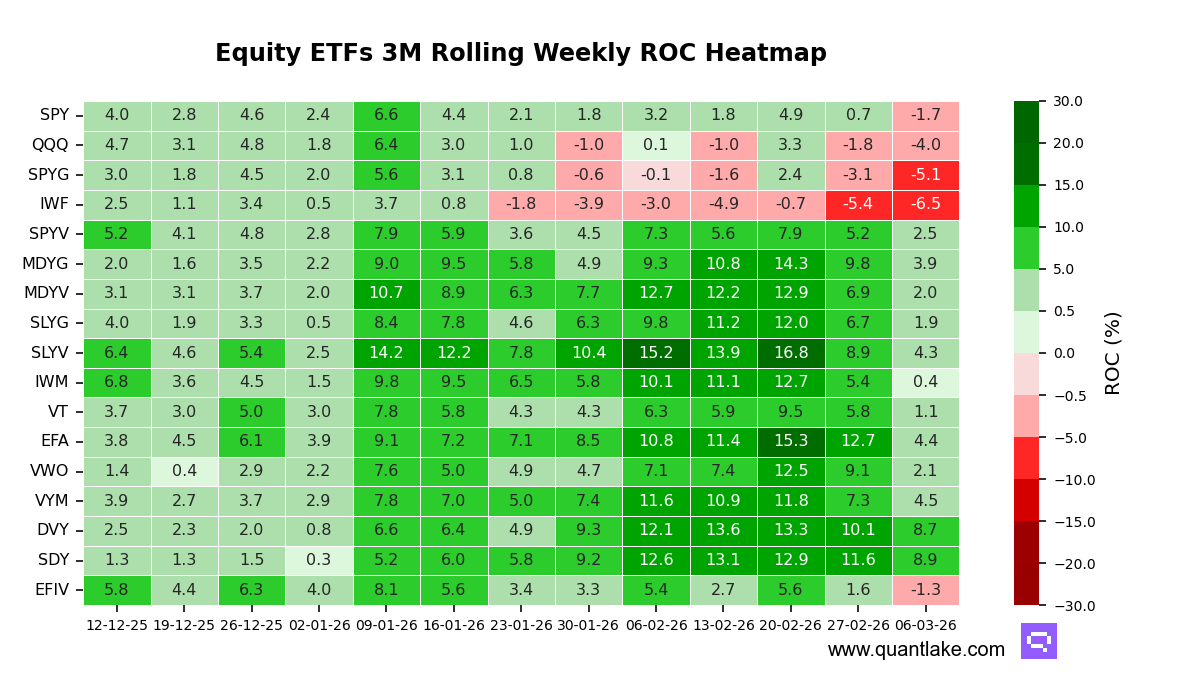

Dividend and value factors continue to set the pace across the ETFs we track, while large-cap growth remains the primary drag. Relative to last week’s rotation-with-cooling setup, this week tightened into a more uniform deceleration, with international developed markets slipping back from the front even as income leadership held.

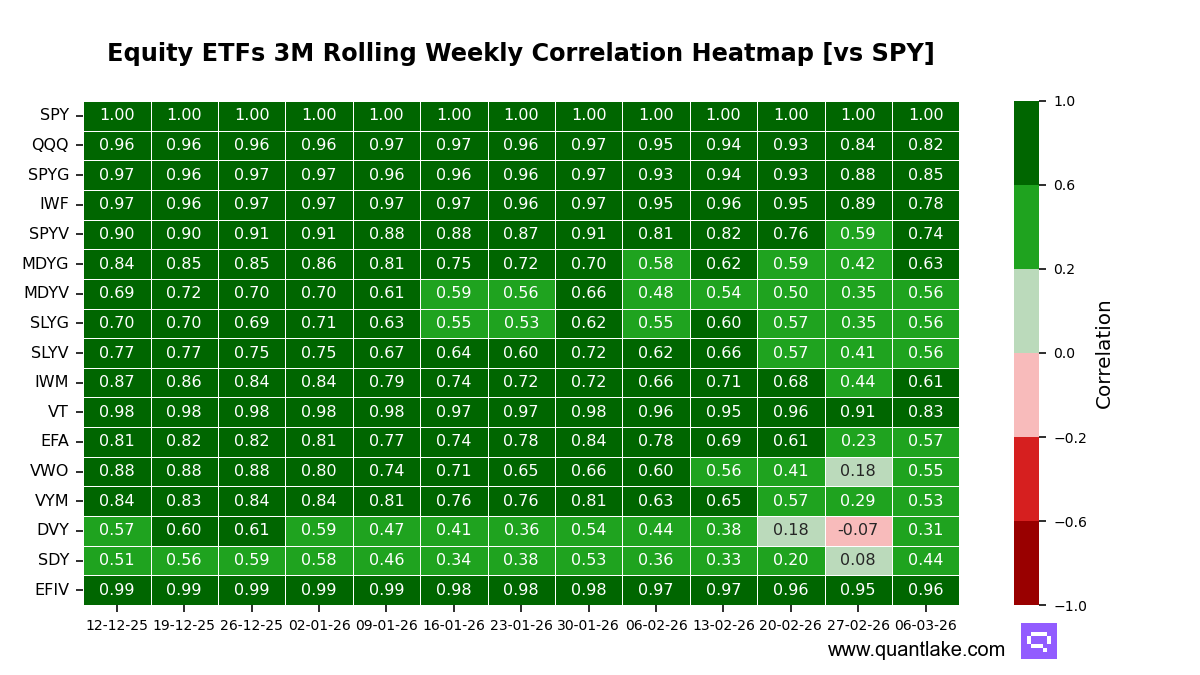

The regime reads less like a single beta tape, as several leaders show decoupling in correlation to SPY versus their 1-year mean alongside sizable alpha contribution. iShares Select Dividend ETF (DVY) shows correlation to SPY of 0.31 versus 0.68, with alpha contribution of 9.5 points. SPDR S&P Dividend ETF (SDY) shows correlation to SPY of 0.44 versus 0.65, with alpha contribution of 10.0 points.

Over the week, breadth deteriorated again: all 17 ETFs saw weaker 3-month trailing momentum. The best relative movers, with the smallest declines in momentum, were iShares Russell 1000 Growth ETF (IWF) at -1.1 points, DVY at -1.4 points, and SPDR Portfolio S&P 500 Growth ETF (SPYG) at -2.0 points. The largest declines were iShares MSCI EFA ETF (EFA) at -8.3 points, Vanguard FTSE Emerging Markets ETF (VWO) at -7.0 points, and SPDR Portfolio S&P 400 Mid Cap Growth ETF (MDYG) at -5.9 points. SPDR S&P 500 ETF Trust (SPY) and iShares MSCI EFA Value ETF (EFIV) flipped negative.

In level terms, SDY and DVY sit in the top decile, with Vanguard High Dividend Yield ETF (VYM) and EFA in the upper third. Small-cap value and mid-cap growth also sit in the upper third, while QQQ, SPYG, and IWF cluster in the bottom decile and remain below zero.

Stretch remains contained. No ETF is statistically stretched on our 1-year Z-score lens; SDY is elevated but not extreme at 1.29, while the weakest growth complex remains depressed but not extreme.

Leadership is increasingly idiosyncratic: SDY and DVY pair lower correlation to SPY with large alpha contribution, consistent with diversification improving and wider internal dispersion. At the other end, EFIV shows correlation to SPY of 0.96 versus 0.99 with only 0.5 points of alpha, behaving more like a beta proxy.

Our take: Compared with last week’s rotation framework, this week’s unanimous deceleration extends the cooling impulse while keeping dividend-led leadership anchored in alpha rather than broad beta.

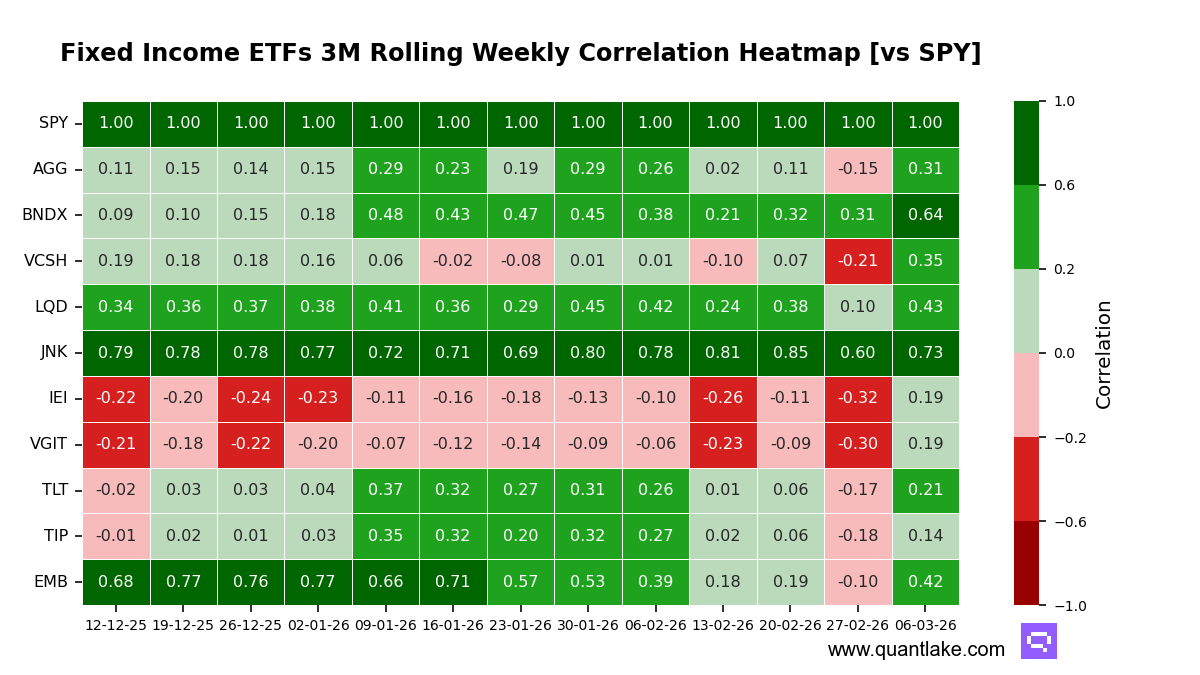

Duration remained the momentum anchor across our fixed income universe, while credit continued to sit in the slipstream. Relative to the prior week’s baseline, the tape shifted from a duration-led advance to a more uniform cooling, with curve leadership intact but less forceful.

Linkage to the broad equity benchmark stayed a key separator, and the correlation profile read more risk-on than the prior snapshot implied for the rate complex. iShares 20+ Year Treasury Bond (TLT) now shows a positive 0.21 correlation versus a -0.10 one-year mean, a convergence that reduces its hedging character. SPDR Bloomberg High Yield Bond (JNK) remained the most equity-sensitive sleeve at 0.73 versus a 0.74 mean, keeping upside participation high while limiting drawdown protection.

This week’s breadth deteriorated sharply versus the prior week. The best relative movers were iShares TIPS Bond (TIP) flat, Vanguard Short-Term Corporate Bond (VCSH) at -0.3 points, and TLT at -0.4 points, each posting the smallest decelerations. The largest declines were iShares JPMorgan USD Emerging Markets Bond (EMB) at -1.7 points, JNK at -1.0 points, and Vanguard Total International Bond (BNDX) at -0.9 points. No tracked fixed income ETF flipped sign.

Leadership by level remained duration-heavy, with TLT in the top decile and TIP in the upper third. iShares Core US Aggregate Bond (AGG) and VCSH sat mid-pack, while JNK and iShares iBoxx $ Investment Grade Corporate Bond (LQD) clustered in the lower half.

Statistical stretch stayed contained. No constituent sat near a statistical ceiling or floor, with the widest deviation at VCSH on a -1.27 z-score, consistent with mild normalization pressure rather than an extreme. Most funds remained well below their 12-month momentum peaks, led by TLT at 6.8 points off its high and JNK at 6.4 points off its high.

Attribution leaned idiosyncratic even as correlations rose. TLT paired low beta at 0.25 with a 1.8-point alpha contribution, while AGG and TIP each carried 1.3 points of alpha with near-zero beta. JNK looked more like a beta proxy, combining the highest correlation with the smallest alpha contribution at 0.6 points, supporting upside participation but offering limited hedging value in equity drawdowns.

Our take: The prior week’s duration-rotation framework extends, but this week’s broad deceleration argues for treating leadership as intact yet less energetic, with credit’s lag now more about internal cooling than a clean handoff back to spread product.