.png)

Daily SPY Candlestick: Piercing Line

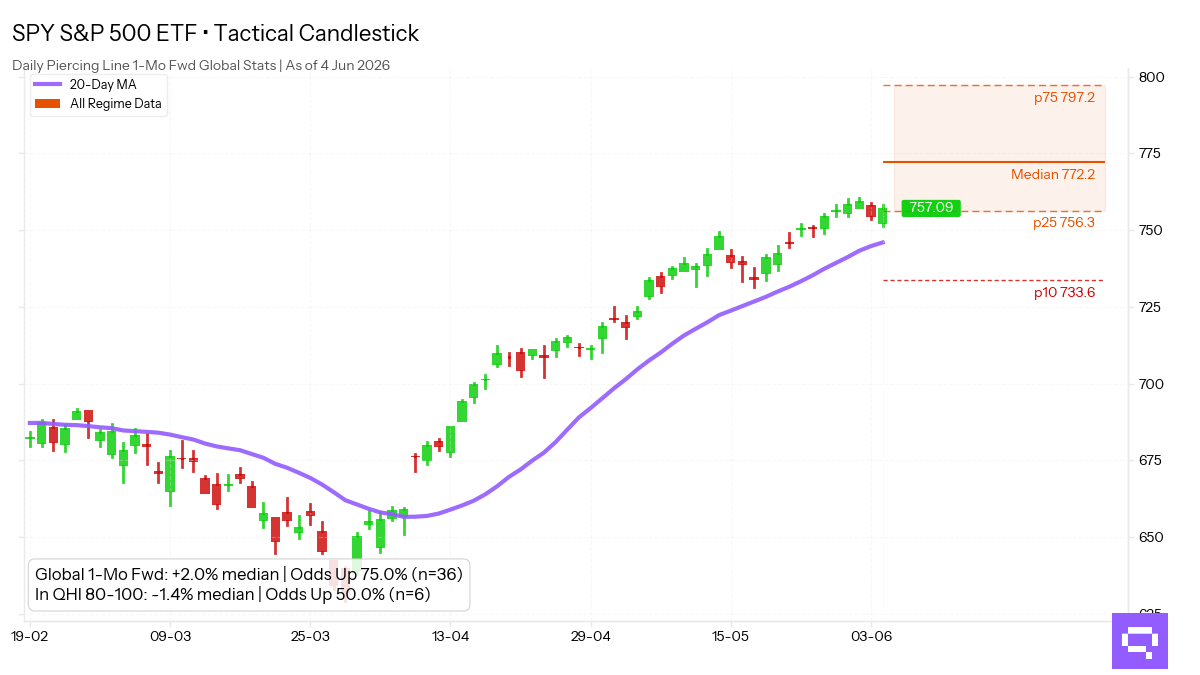

Piercing Line in Extreme Greed: SPY Up Rate Falls to 50% — 25 Points Below the Global Baseline

SPY closed Thursday with a Piercing Line (+0.4%), a bullish reversal signal in which buyers reclaim much of the prior bearish candle and show downside pressure fading.

Across 36 occurrences since 2009, the pattern resolved higher one month later 75.0% of the time, with a 2.0% median return and a 1.87 Sharpe, which places it in the stronger end of bullish reversal profiles without an unusual tail shape. The central spread stayed constructive, with outcomes typically ranging from -0.1% to +5.3% and the full sample extending from -5.8% to +10.4%, so the historical record favored gains while still allowing for ordinary downside variation.

In Quantlake Herd Index (QHI) Extreme Greed conditions, a regime that reflects crowd sentiment at its most stretched, the pattern's 1-month up rate fell to 50.0% and the median outcome dropped to -1.4%, while the Sharpe flattened to 0.00, so the historical risk-adjusted edge narrowed in this setting. With only 6 observations in this regime, treat all regime statistics as indicative only. Taken together, the Extreme Greed subset was much less constructive than the full sample and did not preserve the broader pattern's favorable profile.

Note: limited sample size (n<100) for moment stability.

Warning: low sample (n<30), statistical significance is reduced.

The full QHI historical series since September 1, 2009 is available via the Quantlake API for systematic integration. Learn more about the QHI methodology →

Data: 4 Jun 2026 · Daily Time Scale.

Romain Gandon

CEO, Quantlake

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Definitions

Quantlake Herd Index (QHI)

The Quantlake Herd Index (QHI) is a proprietary cross-asset behavioral sentiment composite ranging from 0 to 100 that measures extremes in investor psychology across the U.S. financial system.

It aggregates signals from U.S. equity momentum and breadth, equity market concentration dynamics, credit market risk appetite (high-yield vs investment-grade demand), implied volatility conditions, and credit spread behavior. These inputs are normalized into a single behavioral risk barometer reflecting the balance between risk-averse and risk-on investor behavior.

Because markets are influenced by behavioral biases, sentiment extremes frequently precede mean reversion in forward returns.

QHI Regimes

0–20: Extreme Fear

20–40: Fear

40–60: Neutral

60–80: Greed

80–100: Extreme Greed

Statistical Terms

Median

The midpoint of the return distribution — 50% of outcomes fell above and 50% below this value. Less sensitive to extreme outliers than the average.

p25 / p75 (Interquartile Range)

The range within which the middle 50% of historical outcomes fell. p25 marks the 25th percentile (bottom of the range); p75 marks the 75th percentile (top). A tighter range indicates a more predictable pattern; a wide range reflects high dispersion.

p10 / p90 (Tail Interval)

The range encompassing the middle 80% of historical outcomes. P10 represents the 10th percentile (the "downside" threshold), while P90 represents the 90th percentile (the "upside" threshold). Unlike the Interquartile Range, this metric captures the shoulders of the distribution, providing a clearer view of potential tail risk and extreme performance potential.

Skew (γ1 — Skewness)

Measures the asymmetry of the return distribution. A negative skew (γ1 < 0) signals a left-tailed distribution — most outcomes cluster on the positive side, but the rare negative outcomes can be severely large. A positive skew (γ1 > 0) is the opposite.

Kurt (γ2 — Excess Kurtosis)

Measures tail density relative to a normal distribution. A high positive value (Leptokurtic) indicates fat tails — extreme events occur more frequently than a normal distribution would predict. A negative value (Platykurtic) indicates thinner tails.

Mesokurtic

A kurtosis value typically within a range of -0.5 to +0.5, consistent with a normal (Gaussian) distribution. Tail risk is neither elevated nor suppressed relative to standard statistical models.

Gaussian (Normal Distribution)

The classic bell-curve distribution. When a pattern's moments are described as "consistent with Gaussian expectations," it means tail risk behaves as standard statistical models would predict — no unusual concentration of extreme outcomes.

Sharpe Ratio (annualised)

Measures risk-adjusted return — the average 1-month forward return divided by its standard deviation, scaled to an annual rate (×√12). A ratio above 1.0 indicates strong return per unit of risk; below 0.5 is weak; negative means the average outcome was a loss. It does not capture skewness or tail risk, so it should be read alongside the distribution metrics above.