.png)

Breadth Holds, Leadership Thins

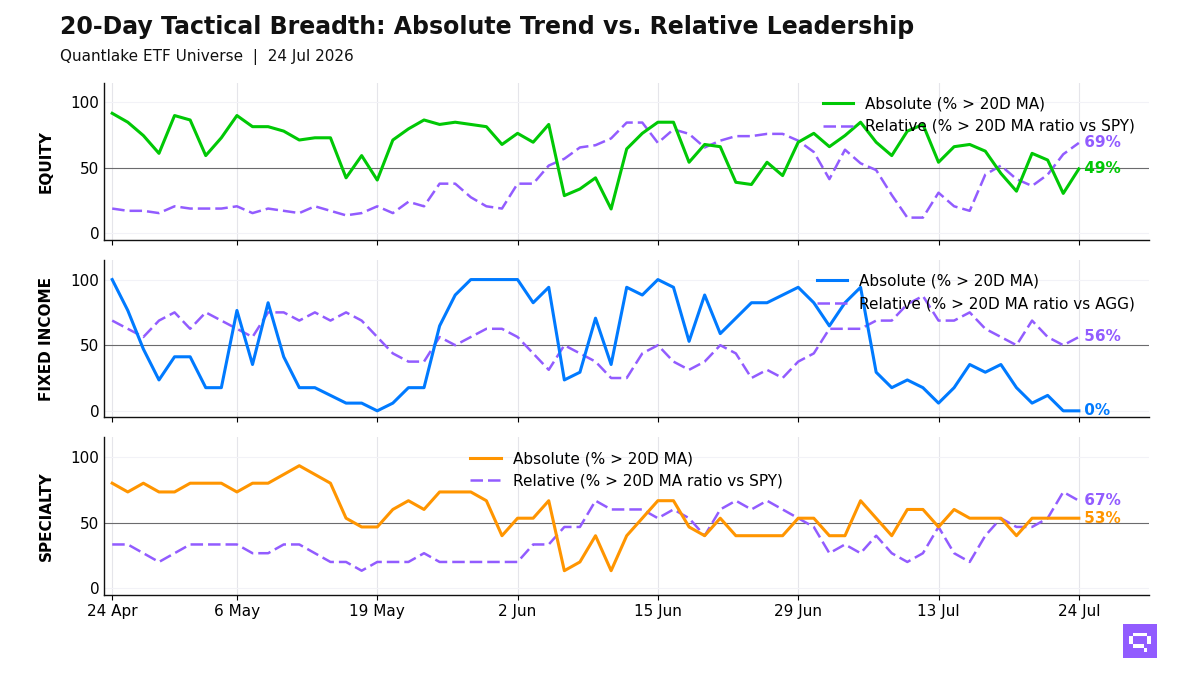

At Tuesday's close, our ETF universe still showed strong price participation, but the dominant regime was benchmark-led rather than broadening. In equity, 56 of 62 ETFs (90%, -6.5pp on the day) held above their 20-day moving average, yet only 16 of 61 (26%, -4.9pp) outperformed their benchmark, leaving a +64pp gap as leadership narrowed to US growth, semiconductors, and selected EM Asia while developed ex-US, low-volatility, and defensive sectors fell behind. Alternatives are even more stretched: 8 of 9 ETFs (89%, +11.1pp on the day) held above their 20-day moving average, but just 1 of 9 (11%, -44.4pp) led its benchmark, a +78pp gap that turns the bounce in commodities and REITs into price recovery without relative sponsorship.

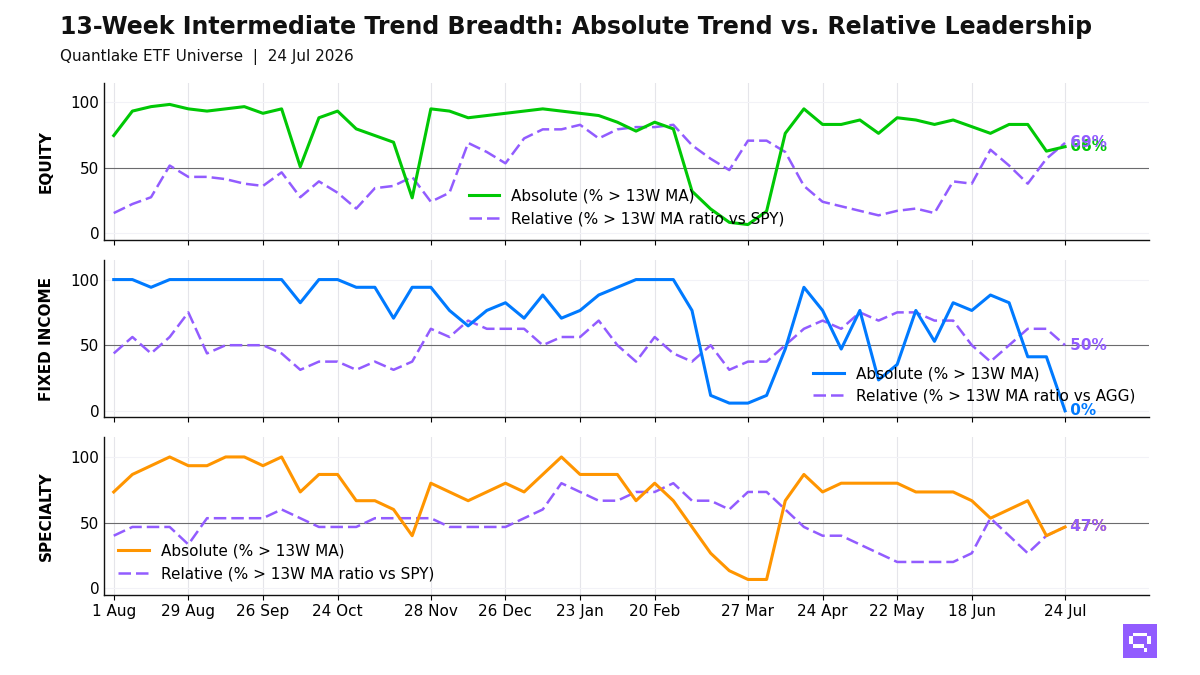

Fixed income is the main offset. All 17 of 17 bond ETFs (100%, unchanged on the day) stayed above their 20-day moving average, and relative breadth improved to 9 of 16 (56%, +6.2pp), led by EM debt, high yield, investment grade, TIPS, and short corporate exposure, while Treasuries, mortgages, and long duration lagged on a rate-sensitive basis; that helps, but conviction stays capped while equity leadership remains concentrated and alternatives keep losing relative ground.

20-Day Tactical Breadth

Key Takeaways

• Emg. Markets VWO lost its 20-day ratio edge even with a positive 20-day relative return, so we read it as fading leadership rather than outright deterioration. Even so, cross-timescale equity leaders still cluster in emerging markets, Taiwan equity, South Korea equity, and US growth-heavy exposure, while Intl Min Vol EFAV, Consumer Staples XLP, and Healthcare XLV have already broken below their 20-day moving averages; with no hovering cluster near key levels, the narrowing is showing up as confirmed breaks rather than indecision.

• TIPS TIP crossed above its 20-day ratio average with a positive 20-day return, which gives the relative move more quality than Short Corporate VCSH, whose cross-up came with a slightly negative 20-day return and looks more like early stabilization. Mortgage-Backed MBB slipped below its ratio average, and the broader cross-timescale split still favors credit over rate-sensitive government bonds and long duration.

• Oil USO and Broad Commodities PDBC both reclaimed their 20-day moving averages, with USO posting the strongest absolute 20-day return in this alert window at +16.0%. That strength is not yet leadership: USO, PDBC, Silver SLV, Global REITs REET, Real Estate VNQ, and Real Estate Sector XLRE are all above their 20-day moving averages while still lagging SPY, Gold GLD moved back below its own average, and only IBIT stands apart as a confirmed relative leader in the bucket.

FEATURED ETF — United States Oil Fund LP USO

Other Technical Signal Events

EQUITY

Absolute Price Signals

Below 20D moving average

• VanEck Gold Miners ETF GDX (20D perf: +11.53%)

• iShares MSCI EAFE Min Vol Factor ETF EFAV (+2.15%)

• Consumer Staples Select Sector XLP (+0.81%)

• Health Care Select Sector XLV (+0.79%)

Relative Strength Signals (vs SPY)

Below 20D moving average

• VanEck Gold Miners ETF GDX (20D relative perf: +3.81%)

• Global X Copper Miners ETF COPX (+3.11%)

• Vanguard FTSE Emerging Markets VWO (+0.70%)

FIXED INCOME

Relative Strength Signals (vs AGG)

Above 20D moving average

• Vanguard Short-Term Corporate Bond VCSH (20D relative perf: unch.)

• iShares TIPS Bond ETF TIP (+0.15%)

Below 20D moving average

• iShares MBS ETF MBB (20D relative perf: +0.13%)

ALTERNATIVES

Absolute Price Signals

Above 20D moving average

• Invesco Optimum Yield Diversified Commodity Strategy No K-1 ETF PDBC (20D perf: +4.88%)

• United States Oil Fund LP USO (+16.00%)

Below 20D moving average

• SPDR® Gold GLD (20D perf: +6.32%)

Relative Strength Signals (vs SPY)

Below 20D moving average

• iShares Silver SLV (20D relative perf: +2.05%)

• SPDR Real Estate Select ETF XLRE (+0.32%)

• iShares Global REIT ETF REET (unch.)

• Vanguard Real Estate ETF VNQ (-0.81%)

Romain Gandon

CEO, Quantlake

Disclaimer: This report is for informational and educational purposes only and does not constitute investment advice.