.png)

Alt ETF Momentum Broadens as Real Assets Lead, Crypto Lags

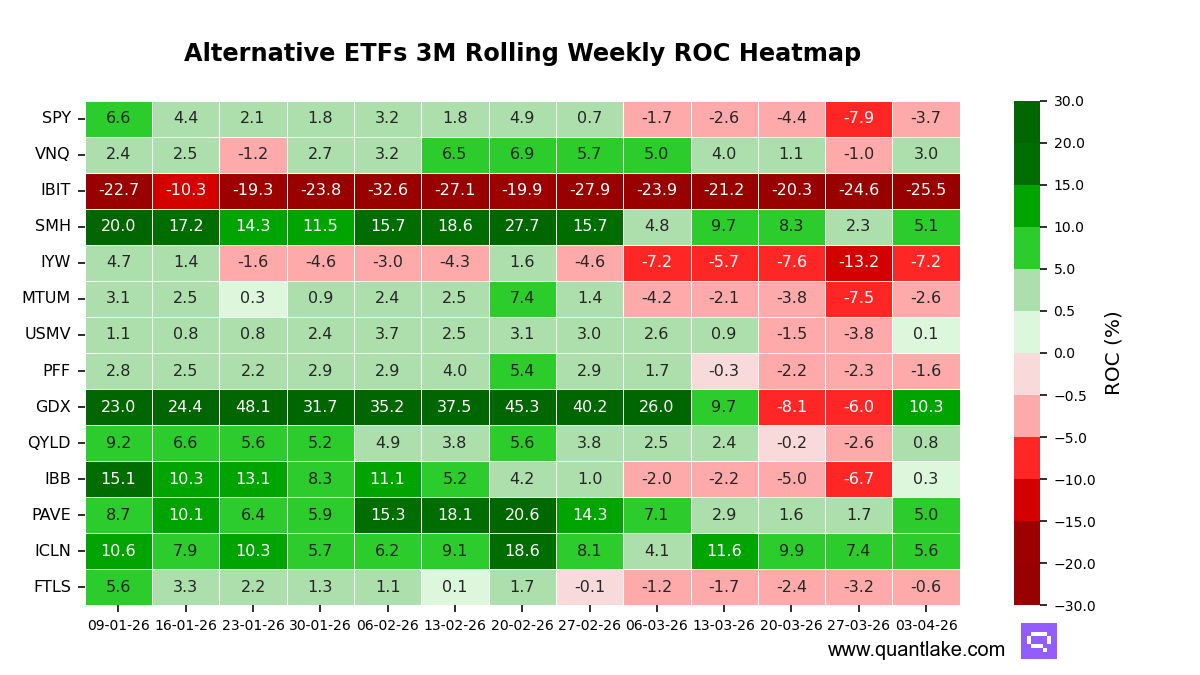

Momentum leadership across the alternative ETFs we track broadened this week, with real assets and defensive carry moving up the stack while crypto remained the clear laggard. Relative to the prior week’s narrow, defensive leadership, the tape looked less one-sided as more constituents registered momentum acceleration. Dispersion remains pronounced, but it is now defined more by a single outlier on the downside than by widespread deterioration.

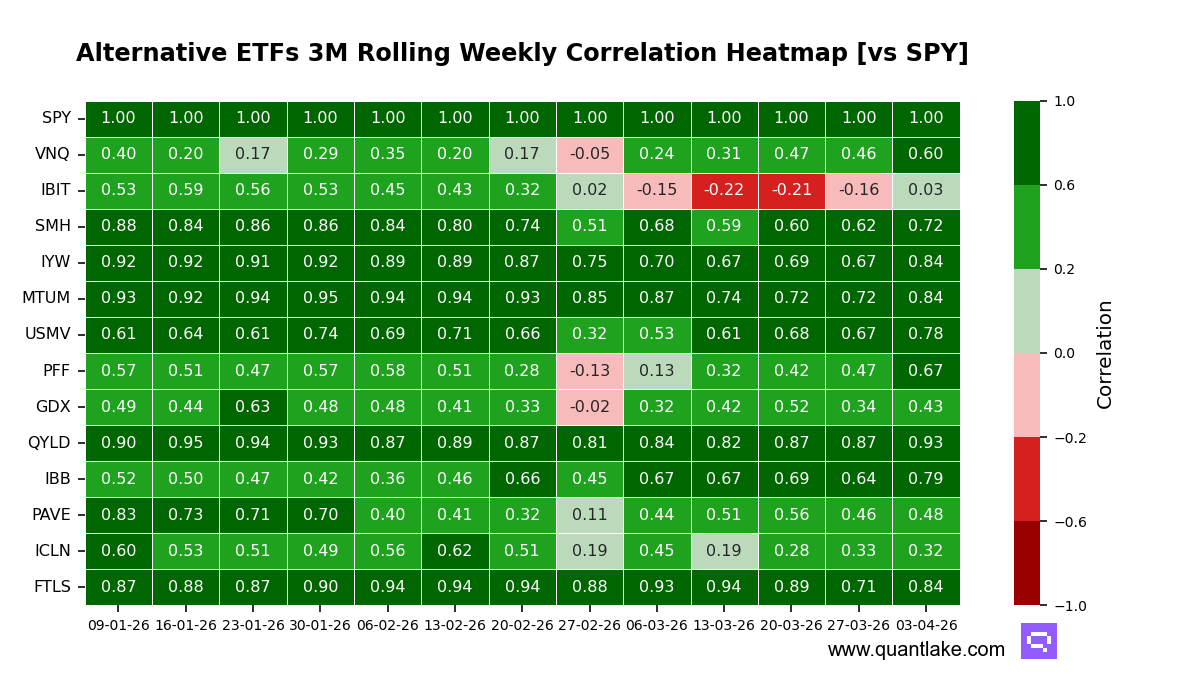

Correlation dynamics continue to separate diversifiers from equity-sensitive proxies. iShares Global Clean Energy shows correlation to the broad equity benchmark at 0.32 versus a 0.56 one-year mean, alongside a 7.7-point alpha contribution, consistent with improved decoupling. Global X U.S. Infrastructure Development also sits below its 1-year mean correlation at 0.48 versus 0.80, with 8.8 points of alpha, keeping leadership more idiosyncratic than beta-led.

This week, breadth strengthened versus the previous read: 12 of 14 ETFs posted higher three-month trailing momentum, and five funds flipped positive. VanEck Gold Miners led the strongest accelerations at +16.3 points, iShares Biotechnology followed at +7.0 points, and iShares U.S. Technology added +6.0 points. The weakest relative movers were iShares Global Clean Energy at -1.8 points, iShares Bitcoin Trust at -0.9 points, and iShares Preferred and Income Securities at +0.7 points.

In level terms, Gold Miners and Clean Energy sit in the top decile, with VanEck Semiconductor also in the upper tier. Infrastructure and Vanguard Real Estate sit in the upper third, while iShares Bitcoin Trust remains in the bottom decile and iShares U.S. Technology stays in the lower half despite this week’s rebound in momentum.

Stress looks contained across the complex: no ETF shows a Z-score beyond 2 in absolute terms. Clean Energy, Gold Miners, and Bitcoin all screen below their own one-year averages on Z-score terms, pointing to depressed positioning rather than a statistical ceiling, while Semiconductors remain far from their one-year peak despite a positive current reading.

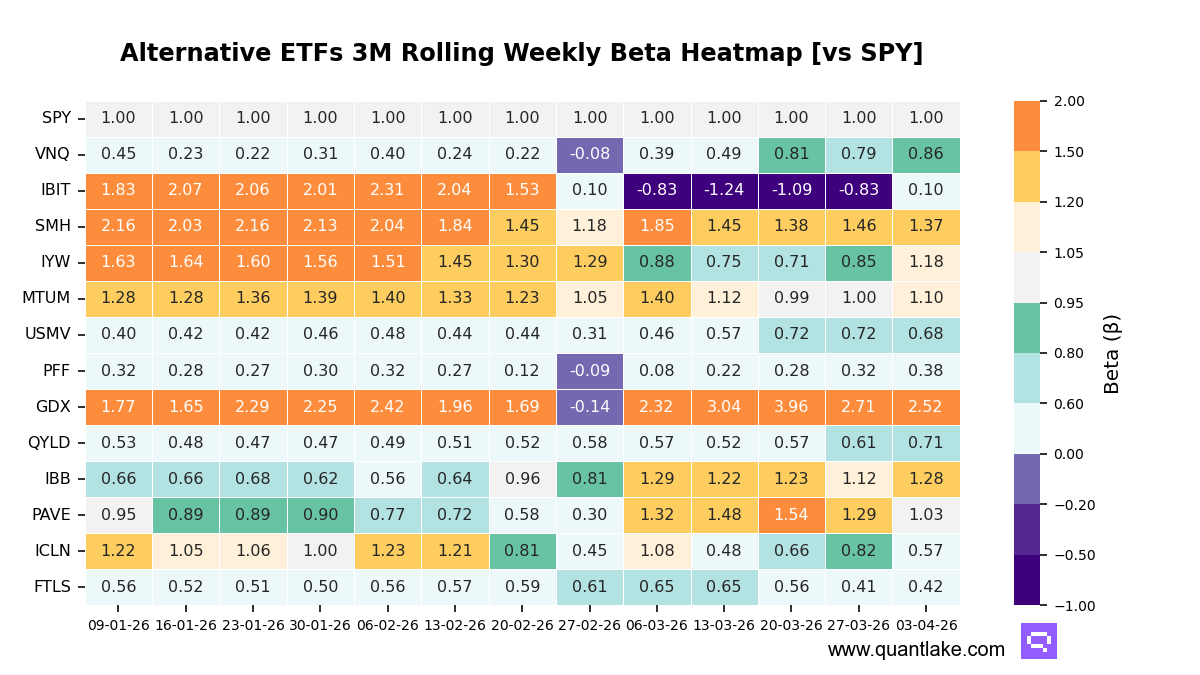

Attribution reinforces a mixed leadership profile. Gold Miners pair a 0.43 correlation to the broad equity benchmark with a 19.6-point alpha contribution, suggesting leadership that is not purely benchmark-driven even with elevated beta. Bitcoin’s correlation is near zero at 0.03 versus a 0.27 mean, but the -25.1-point alpha contribution and high momentum volatility keep it isolated rather than a stable diversifier.

Our take: last week’s message of narrow, defensive leadership looks less restrictive as breadth improved and multiple funds flipped positive, even as crypto remains the dominant source of downside dispersion.