.png)

Tactical Trends: Cyclicals Rejoin as Equities Stay Benchmark-Led

Price participation broadened faster than relative confirmation

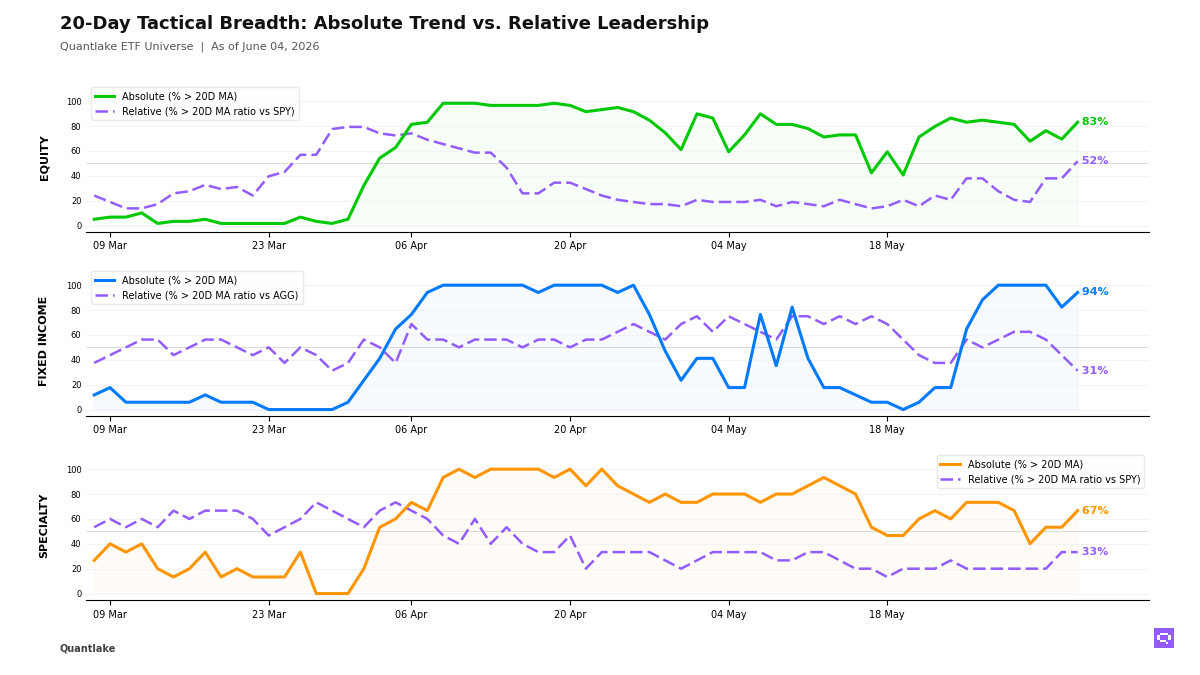

At the close, equity price participation rebounded across our ETF universe, with 49 of 59 ETFs (83%, +13.6pp) above their 20-day moving average and 30 of 58 (52%, +13.8pp) outperforming the S&P 500 SPY. US cyclicals, smaller caps, Asia-Pacific equity, and selective healthcare drove that expansion, with Dow Jones DIA and Healthcare XLV moving into relative leadership. The +31pp gap between absolute and relative breadth keeps equities in a benchmark-led regime rather than a fully shared advance.

In fixed income, price participation broadened even as internal leadership weakened, with 16 of 17 ETFs (94%, +11.8pp) above their 20-day moving average but only 5 of 16 (31%, -12.5pp) outperforming the Aggregate Bonds AGG. Credit, munis, and long duration carried the relative side as Treasuries, mortgages, and international aggregate lagged, leaving bonds in a strongly benchmark-led configuration with a +63pp abs/rel gap.

Specialty price recovery widened, but only a narrow group beat the S&P 500 SPY, with semiconductors, momentum, and clean energy leading while biotech, real estate, crypto proxies, and precious metals failed to confirm. In commodities, Copper CPER improved on a relative basis versus the S&P 500 SPY as Oil USO fell below its 20-day moving average, leaving specialty and commodities in a selective rotation rather than a coordinated cyclical phase.

20-Day Tactical Breadth

Key Takeaways

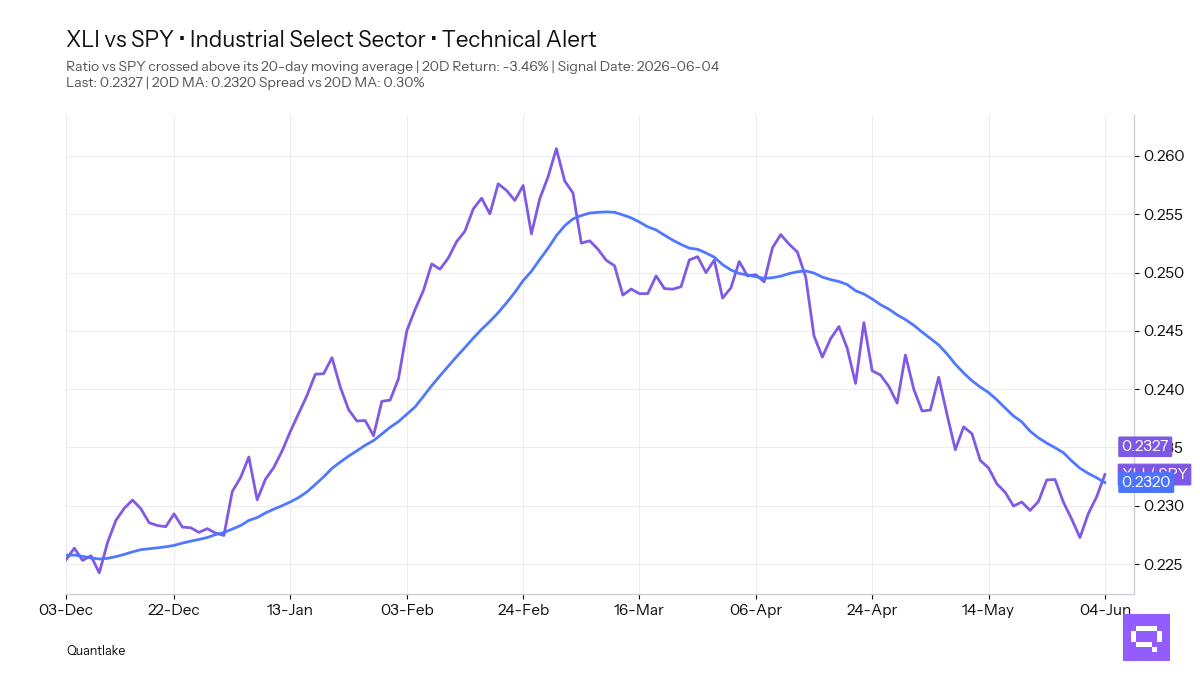

• Industrials XLI with a -3.46% period relative return versus SPY crossed above its 20-day ratio moving average. That move sits in the same early repair cluster as Small-Cap IJR, Russell 2000 IWM, and Intl Momentum IMTM, where the ratio break improved but trailing 20-day relative performance remained negative. We keep the deeper cross-timescale leadership concentrated in US growth and Asia exporters, so the equity rotation broadened without displacing the established leaders.

• Fixed income split internally rather than moving in one direction. Global Bonds BNDX and Mortgage-Backed MBB crossed below their ratio moving averages versus Aggregate Bonds AGG. 3-7yr Treasuries IEI and Int. Treasuries VGIT moved back above their 20-day moving averages in price. That mix marks rate-sensitive stabilization with benchmark outperformance confined to selective credit, munis, EM debt, and long duration.

• Biotechnology IBB and Real Estate VNQ moved back above their 20-day moving averages. They stayed in the divergent group that recovered in price without beating the S&P 500 SPY. Semiconductors SMH, momentum, and clean energy held the cleaner relative leadership profile across specialty. In commodities, Copper CPER crossed above its 20-day ratio moving average versus the S&P 500 SPY. Oil USO crossed below its 20-day moving average. The commodity tape stayed split rather than unified across inflation-sensitive exposure.

FEATURED ETF — Industrial Select Sector XLI vs SPY

Other Technical Signal Events

EQUITY

↗ Price breakouts (cross-up 20D MA)

• EWU - iShares MSCI United Kingdom ETF · 20D perf: -1.18%

• IQLT - iShares MSCI Intl Quality Factor ETF · -1.02%

• EWG - iShares MSCI Germany ETF · -0.92%

• XLRE - SPDR Real Estate Select ETF · -0.76%

• JEPI - JPMorgan Equity Premium Income ETF · -0.67%

• VGK - Vanguard FTSE Europe · -0.38%

• XLF - Financial Select Sector · +0.68%

• ACWV - iShares MSCI Global Min Vol Factor ETF · +0.74%

↘ Price breakdowns (cross-down 20D MA)

None on the close

↗ Leadership gains (cross-up 20D MA vs SPY)

• XLI - Industrial Select Sector · 20D relative perf: -3.46%

• SLYG - SPDR® S&P 600 Small Cap Growth ETF · -2.98%

• IJR - iShares Core S&P Small-Cap ETF · -2.14%

• IMTM - iShares MSCI Intl Momentum Factor ETF · -1.86%

• IWM - iShares Russell 2000 ETF · -1.31%

• URTH - iShares MSCI World ETF · -0.64%

• DIA - SPDR Dow Jones Industrial Average ETF · +0.41%

• XLV - Health Care Select Sector · +1.38%

↘ Leadership losses (cross-down 20D MA vs SPY)

None on the close

FIXED INCOME

↗ Price breakouts (cross-up 20D MA)

• VGIT - Vanguard Intermediate-Term Treasury · 20D perf: -0.45%

• IEI - iShares 3-7 Year Treasury Bond ETF · -0.43%

↘ Price breakdowns (cross-down 20D MA)

None on the close

↗ Leadership gains (cross-up 20D MA vs AGG)

None on the close

↘ Leadership losses (cross-down 20D MA vs AGG)

• BNDX - Vanguard Total International Bond · 20D relative perf: +0.27%

• MBB - iShares MBS ETF · unch.

SPECIALTY

↗ Price breakouts (cross-up 20D MA)

• IBB - iShares Biotechnology ETF · 20D perf: -1.40%

• VNQ - Vanguard Real Estate ETF · -1.02%

↘ Price breakdowns (cross-down 20D MA)

None on the close

↗ Leadership gains (cross-up 20D MA vs SPY)

None on the close

↘ Leadership losses (cross-down 20D MA vs SPY)

None on the close

COMMODITIES

↗ Price breakouts (cross-up 20D MA)

None on the close

↘ Price breakdowns (cross-down 20D MA)

• USO - United States Oil Fund LP · 20D perf: +2.08%

↗ Leadership gains (cross-up 20D MA vs SPY)

• CPER - United States Copper LP · 20D relative perf: +2.58%

↘ Leadership losses (cross-down 20D MA vs SPY)

None on the close

Romain Gandon

CEO, Quantlake

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice. Past performance is not indicative of future results.