.png)

Dividend ETFs Lead as Breadth Cools Across Markets

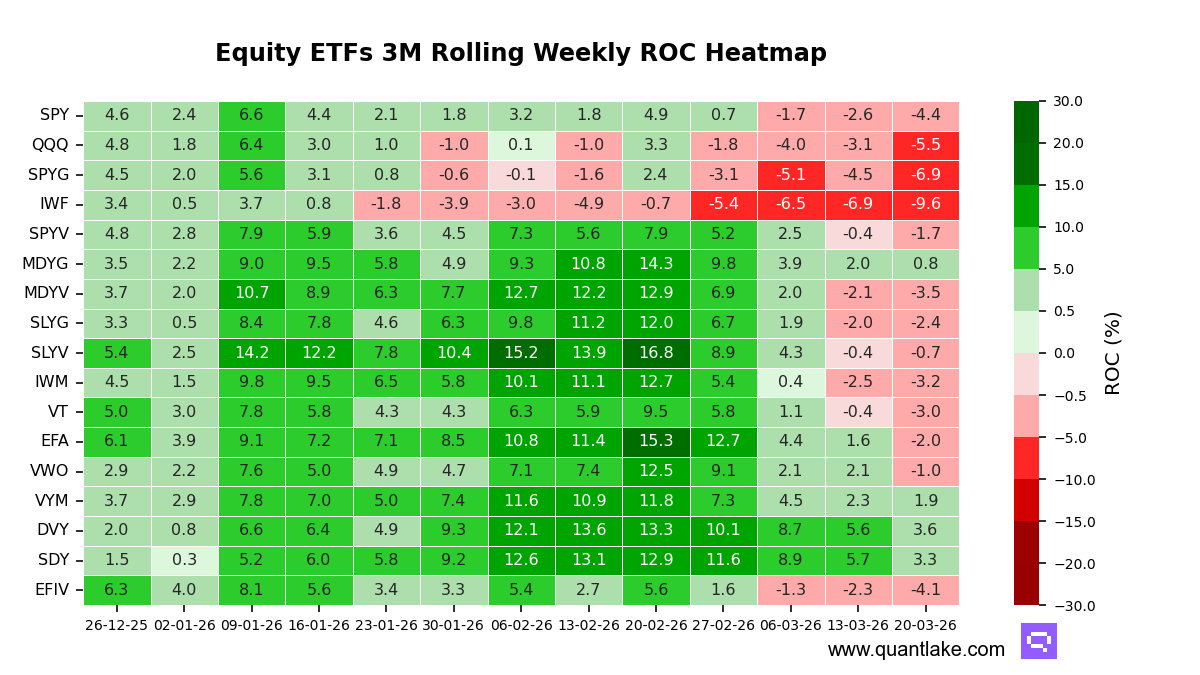

Dividend and income exposures continued to lead our universe, while large-cap growth remained the primary drag. After last week’s small pocket of stabilization in growth, this week reverted to a more uniform cooling across styles and regions, with leadership narrowing further.

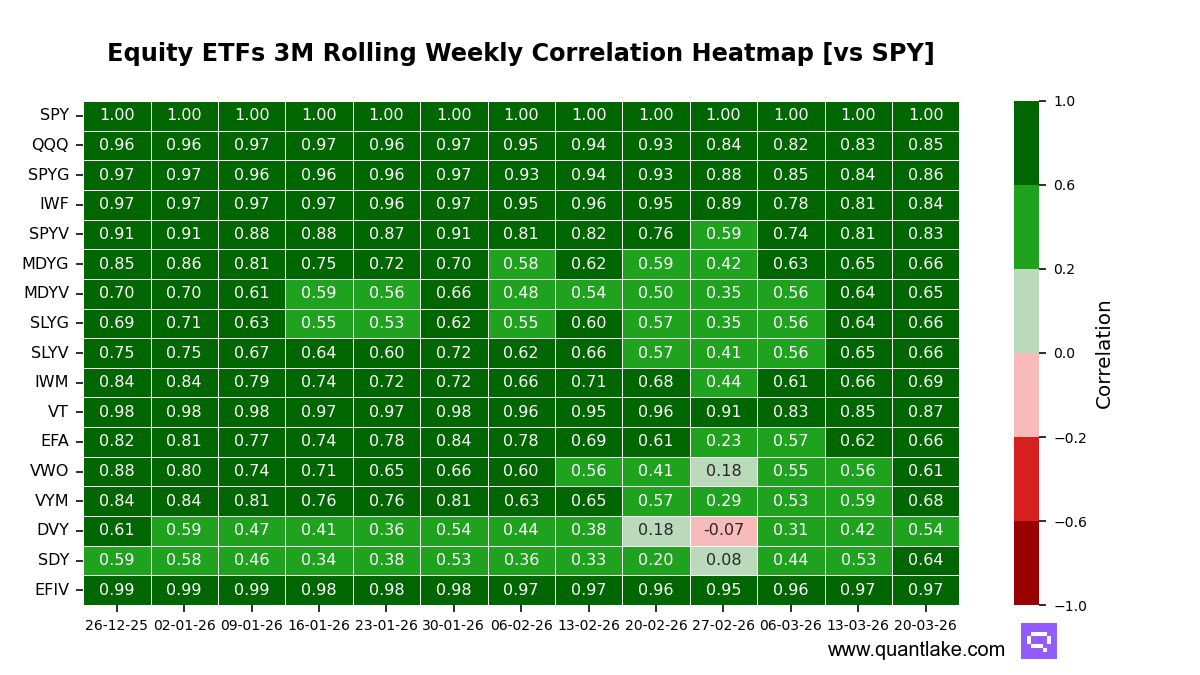

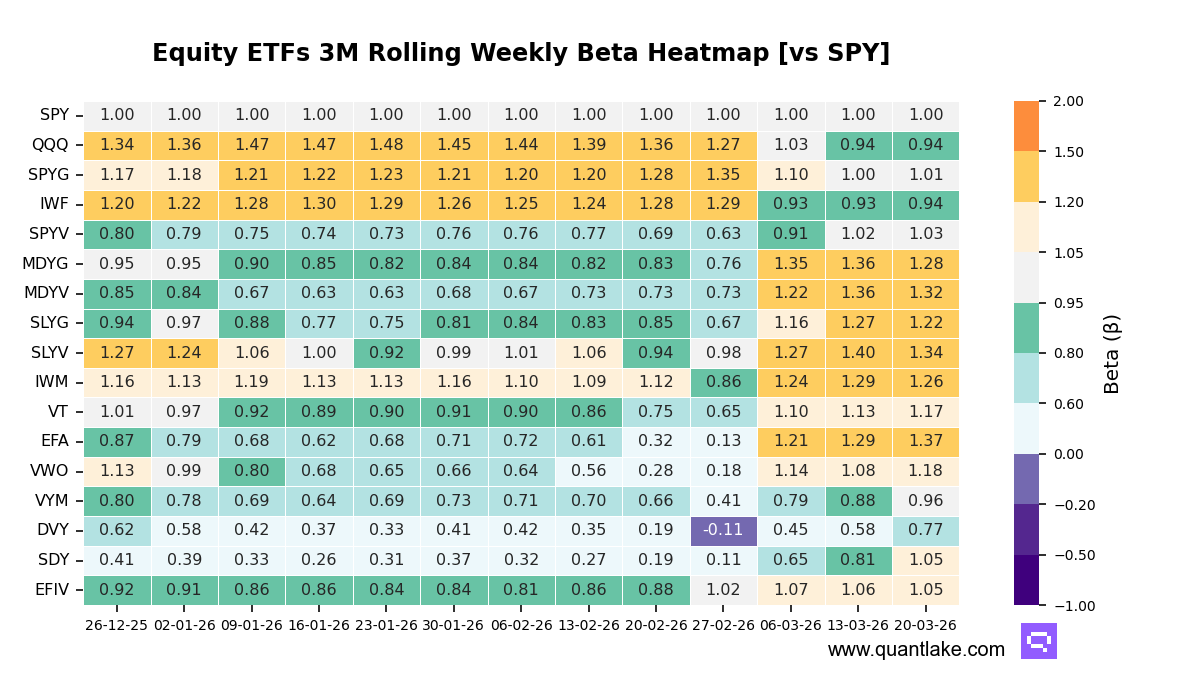

The tape read less like a single beta trade, as key leaders showed lower correlation to SPY than their 1-year mean alongside sizable alpha contribution. iShares Select Dividend ETF (DVY) showed correlation to SPY of 0.54 versus 0.67, with 7.0 points of alpha contribution, and SPDR S&P Dividend ETF (SDY) showed 0.64 versus 0.65 with 7.9 points of alpha.

Over the week, breadth deteriorated across the ETFs we track, with every constituent posting a weaker 3-month trailing momentum read. The weakest were iShares MSCI EAFE ETF (EFA), down 3.6 points, Vanguard FTSE Emerging Markets ETF (VWO), down 3.1 points, and iShares Russell 1000 Growth ETF (IWF), down 2.7 points. EFA and VWO flipped negative.

In level terms, DVY and SDY sat in the top decile, with Vanguard High Dividend Yield ETF (VYM) and SPDR Portfolio S&P 400 Mid Cap Growth ETF (MDYG) in the upper third and the only other names above zero. Large-cap growth remained in the lower half, with Invesco QQQ Trust (QQQ), SPDR Portfolio S&P 500 Growth ETF (SPYG), and IWF clustered near the bottom.

Stretch signals stayed mostly contained, but EFA was statistically depressed on a 1-year Z-score of -2.21 and sat at its 12-month trough, flagging normalization risk rather than a directional call. VWO was depressed but not extreme at -1.59, while DVY and SDY were near neutral versus their own 1-year averages.

Our take: Last week’s dividend-led, alpha-heavy framework extended, but this week’s broad deceleration, and the fresh flips in EFA and VWO, sharpened the breadth warning even as leadership remained relatively differentiated versus SPY.

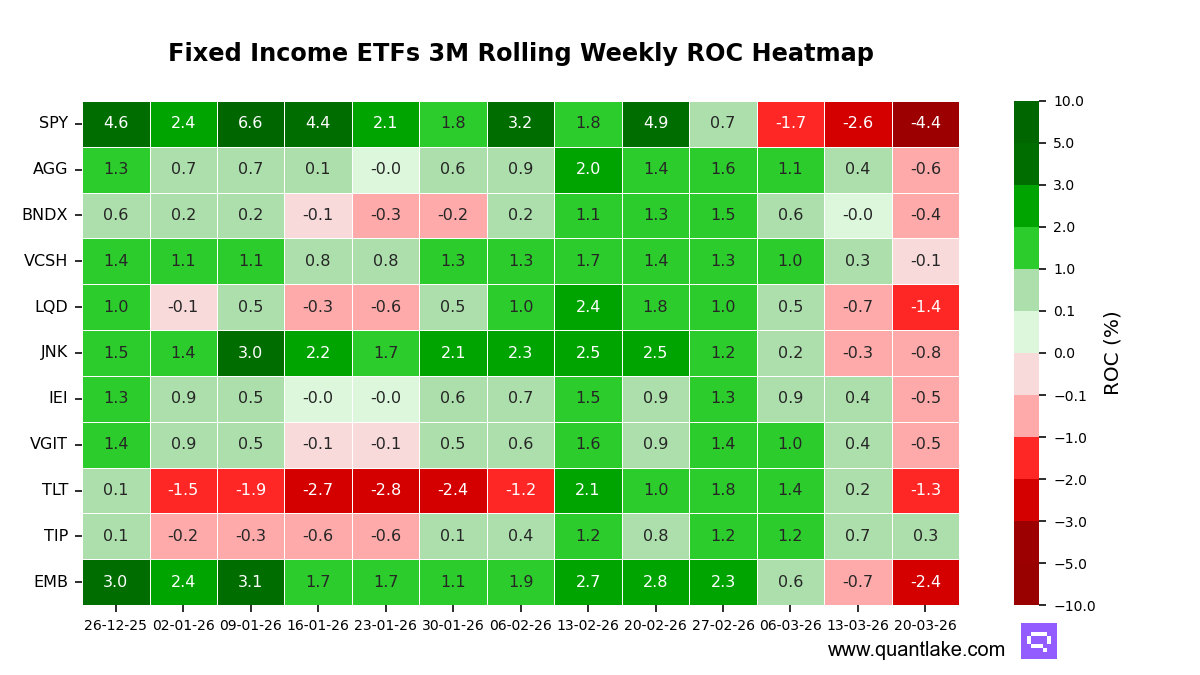

Fixed income momentum is broadly weaker across our universe, with leadership shrinking to a single pocket of positive trailing momentum. Versus last week’s baseline, the tape looks less like a duration-versus-credit split and more like a synchronized cooling across the curve, with sharper slippage at the long end and in emerging-market credit.

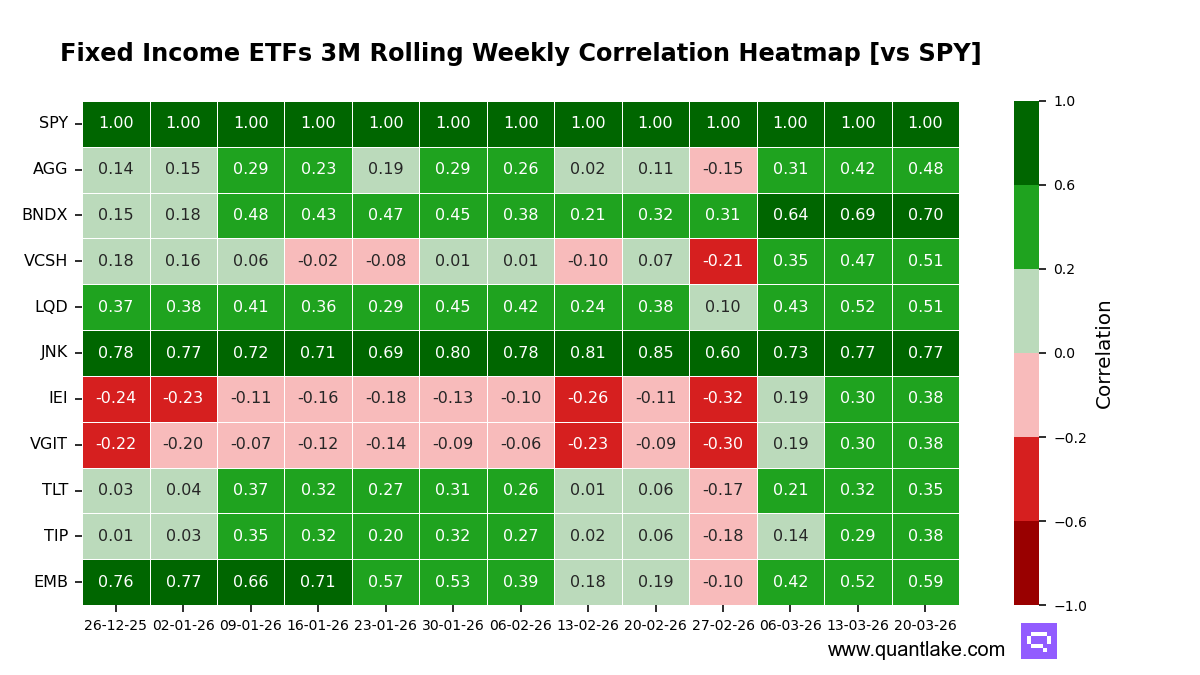

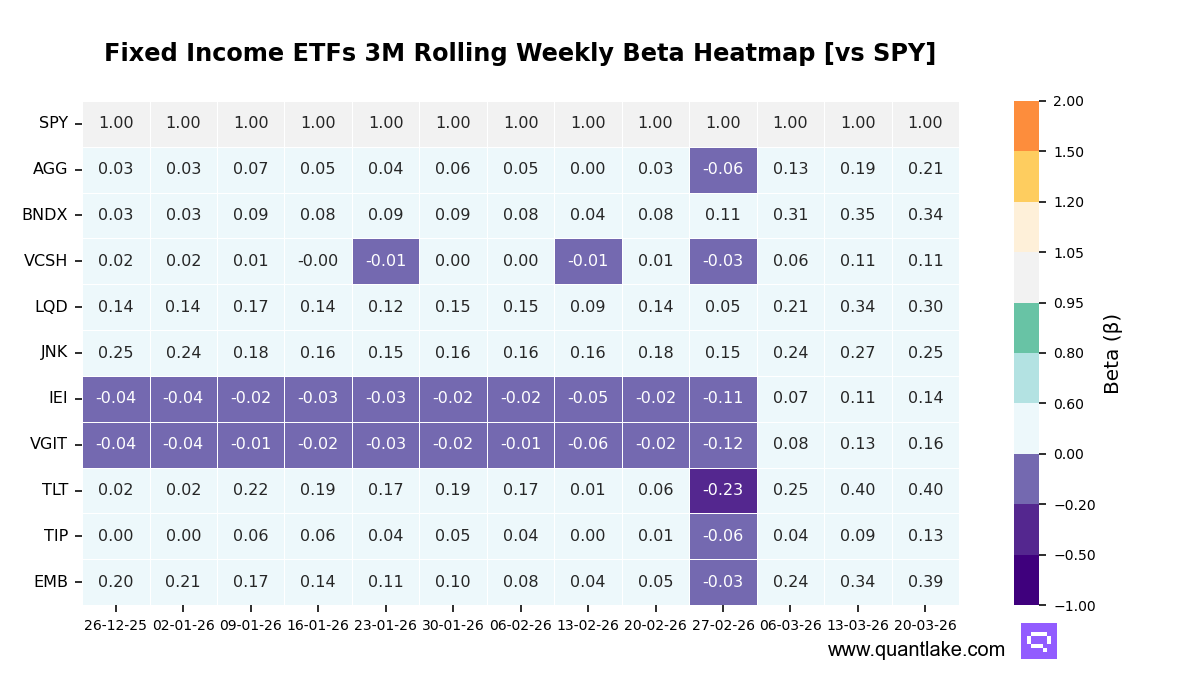

Linkage to the broad equity benchmark remains elevated across most rate-sensitive sleeves, reinforcing a more risk-on profile than their own one-year norms imply. Long-duration Treasuries are the clearest example of that convergence, while high yield remains the most equity-sensitive segment in our set.

Breadth deteriorated versus the prior week: all ETFs we track weakened on a three-month trailing basis. The largest declines were iShares J.P. Morgan USD Emerging Markets Bond ETF (EMB) at -1.7, iShares 20+ Year Treasury Bond ETF (TLT) at -1.5, and iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) at -0.7. AGG, VCSH, IEI, VGIT, and TLT flipped negative.

In level terms, TIP sits alone in the top decile as the only ETF with positive three-month trailing momentum. VCSH and BNDX cluster in the upper third despite being below zero, while VGIT, IEI, and AGG sit mid-pack. LQD and TLT occupy the lower half, and EMB anchors the bottom decile.

Stretch is now a first-order constraint. VCSH screens at a statistical floor with a -2.95 z-score, a setup where mean-reversion pressure can dominate incremental momentum shifts. EMB (-2.48) and IEI (-2.12) are also deeply depressed, and several funds are pinned at their 12-month troughs, including AGG, BNDX, VCSH, LQD, IEI, VGIT, and EMB.

On attribution, leadership looks more beta-aware than internally driven. TLT’s correlation to the broad equity benchmark is 0.35 versus a -0.10 one-year mean, and its alpha contribution is a modest 0.5 points, consistent with reduced hedging value in drawdowns even as upside participation improves when equities advance. JNK’s correlation is 0.77 versus a 0.74 mean, with just 0.3 points of alpha contribution, keeping it firmly in the beta-proxy lane.

Our take: Versus last week, the universal deceleration, multiple flips below zero, and persistent convergence to the broad equity benchmark reinforce the case for treating fixed income leadership as narrower and less defensive.