.png)

Alt ETF Momentum Rotates to Clean Energy & Semis

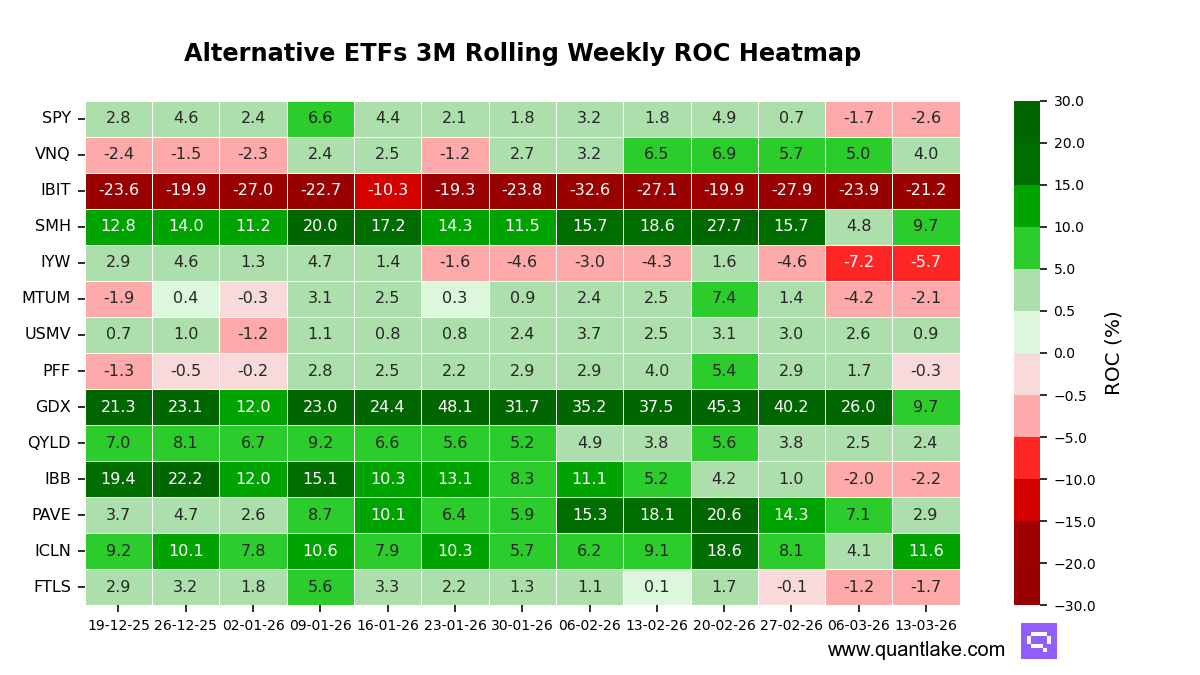

Momentum leadership across the alternative ETFs we track rotated away from the prior week’s real-asset dominance and toward cleaner, more growth-linked sleeves. The tape remains dispersed, but breadth looked less one-way than the previous read, with a clearer split between accelerating leaders and pockets of renewed cooling.

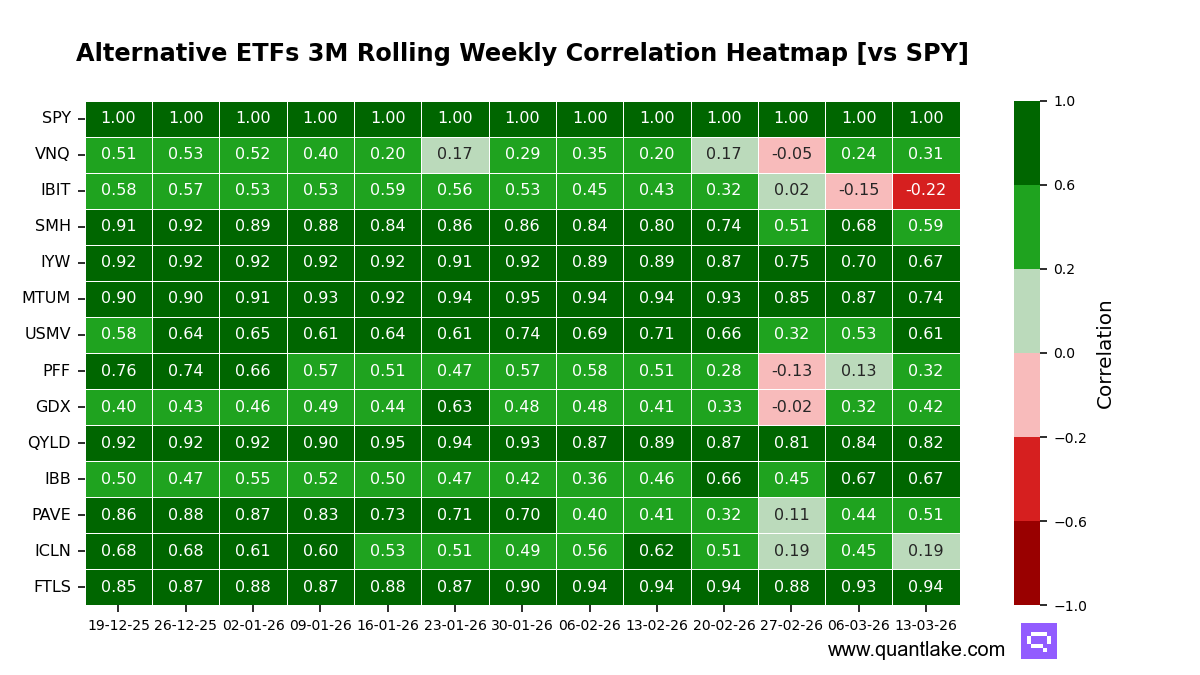

Correlation and attribution continued to argue for a mixed, not monolithic, alternatives regime. iShares Global Clean Energy showed low correlation to the broad equity benchmark at 0.19 alongside a 12.8-point alpha contribution, consistent with more idiosyncratic leadership. VanEck Gold Miners, despite remaining a momentum leader, carried higher equity sensitivity than the prior baseline with correlation at 0.42 and a 17.6-point alpha contribution.

Over the week, breadth improved versus the prior week’s near-universal deterioration, with 5 of 14 ETFs posting stronger 3-month trailing momentum. The strongest accelerations were iShares Global Clean Energy (+7.5 points), VanEck Semiconductor (+4.9 points), and iShares Bitcoin Trust (+2.7 points). The largest declines were VanEck Gold Miners (-16.3 points), Global X U.S. Infrastructure Development (-4.2 points), and iShares Preferred and Income Securities (-2.0 points). Preferreds flipped negative.

Leadership now clusters at the top in Clean Energy, Semiconductors, and Gold Miners, with Real Estate in the upper third. Bitcoin remains in the bottom decile, while US Technology and the Momentum Factor sit in the lower half with negative momentum.

Statistical stretch remains contained, with no ETF at a two-standard-deviation extreme. Gold Miners sits near a 12-month low regime with a -1.51 z-score, framing the latest cooling as normalization risk rather than an overextended unwind.

From an attribution lens, leadership splits between idiosyncratic alpha and equity-sensitive proxies. Clean Energy and Real Estate pair lower correlation with positive alpha, while Semiconductors and Infrastructure carry higher correlation and sizable beta, reading more like equity-linked expressions. Bitcoin’s negative correlation and deeply negative alpha contribution keep it isolated rather than a broad risk proxy.

Our take: the prior week’s real-asset, alpha-led framing looks less dominant as leadership broadens into cleaner and higher-beta sleeves, even as dispersion and selective idiosyncratic alpha remain intact.