.png)

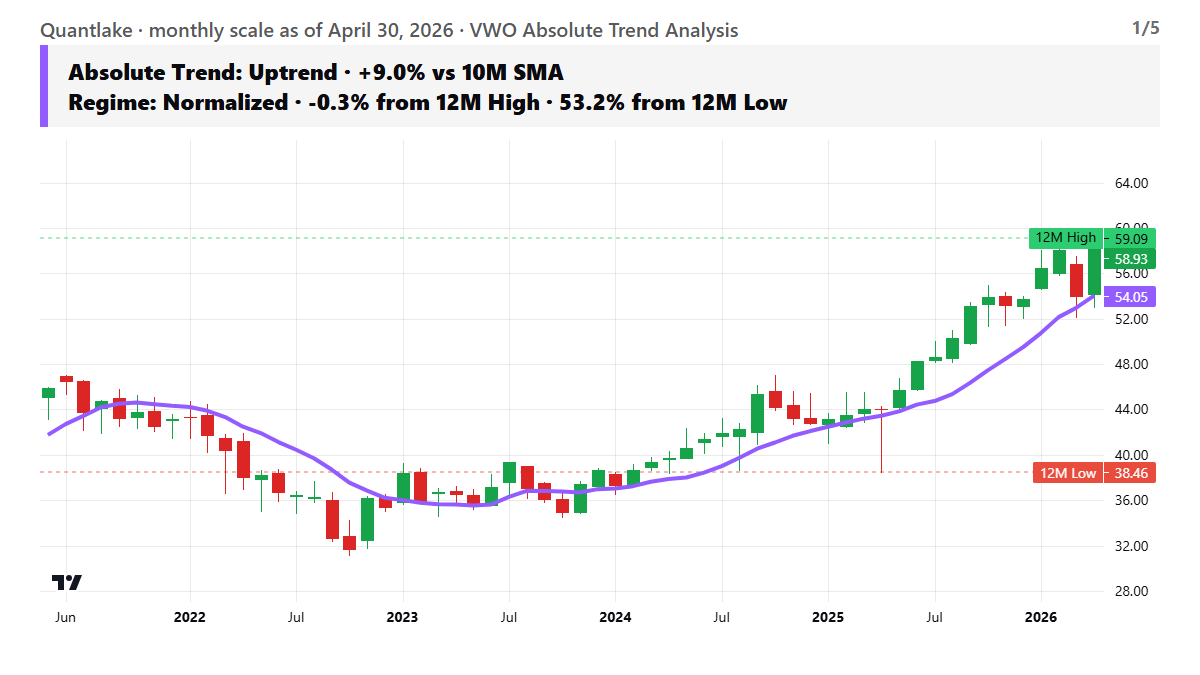

Emerging Tech And Financials Power VWO

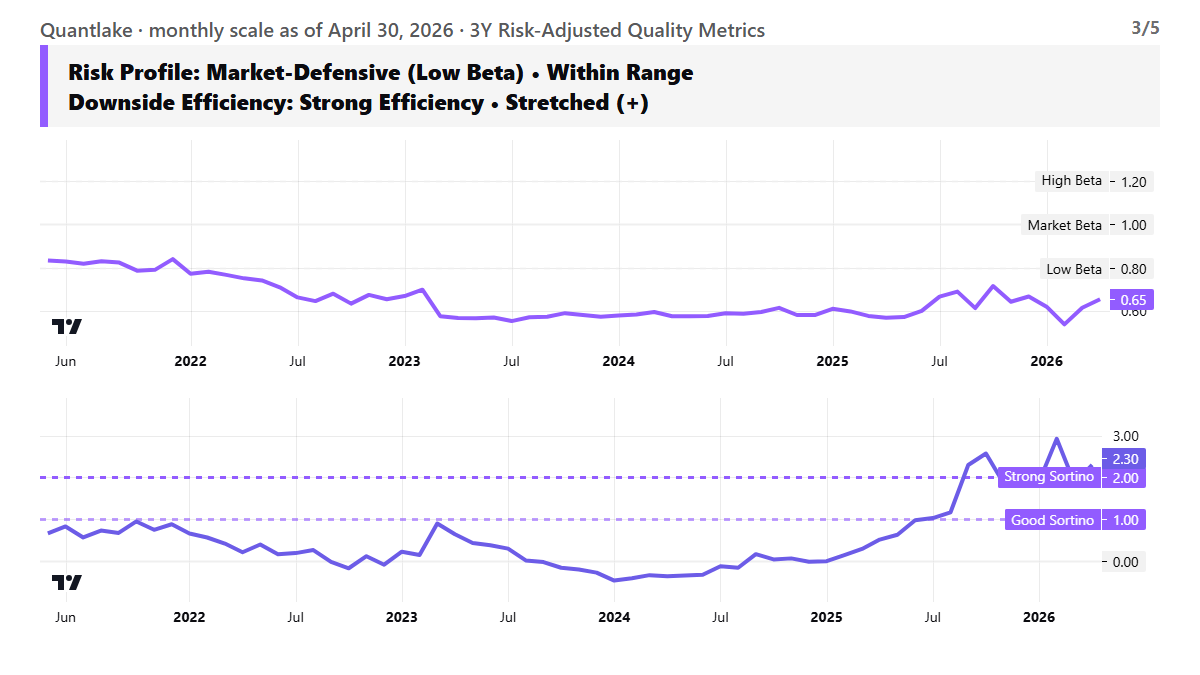

Vanguard FTSE Emerging Markets Index Fund ETF Shares is getting its best support from improving downside efficiency, not a runaway macro tailwind. Rolling 3-year Beta is 0.65, up from 0.62 three months ago, while Sortino ratio is 2.30, improving from 1.90. That combination fits a fund participating in risk assets without taking full market sensitivity.

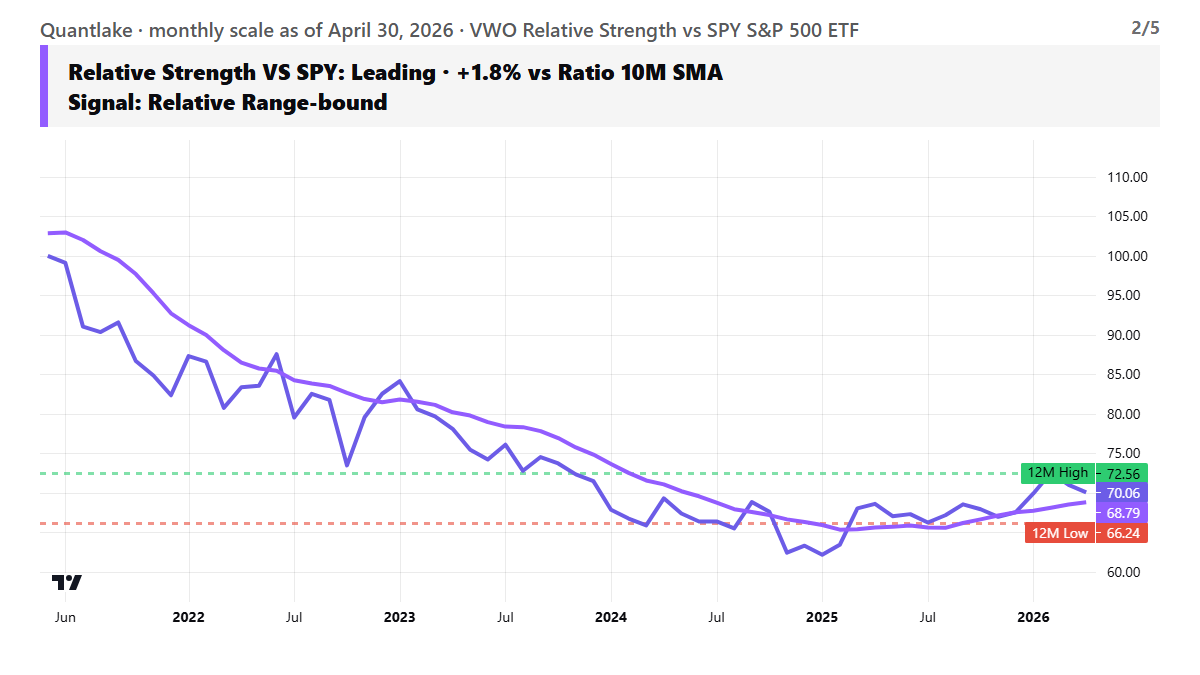

The leadership mix also spans more than one factor. Taiwan Semiconductor Manufacturing (12.8% of the fund's assets) is reinforcing the technology complex through record iPhone-related demand and a new long-dated power agreement that improves capacity visibility. Tencent (3.6%) and Alibaba (2.6%) are tied to firmer domestic artificial intelligence demand and enterprise software adoption in China, while HDFC Bank (1.5%) and China Construction Bank (1.0%) add support from financials as profit trends and credit performance hold up. Relative strength has rolled 3.4% off its recent peak even as it stays above its long-term average. That says leadership is intact, though no longer accelerating.

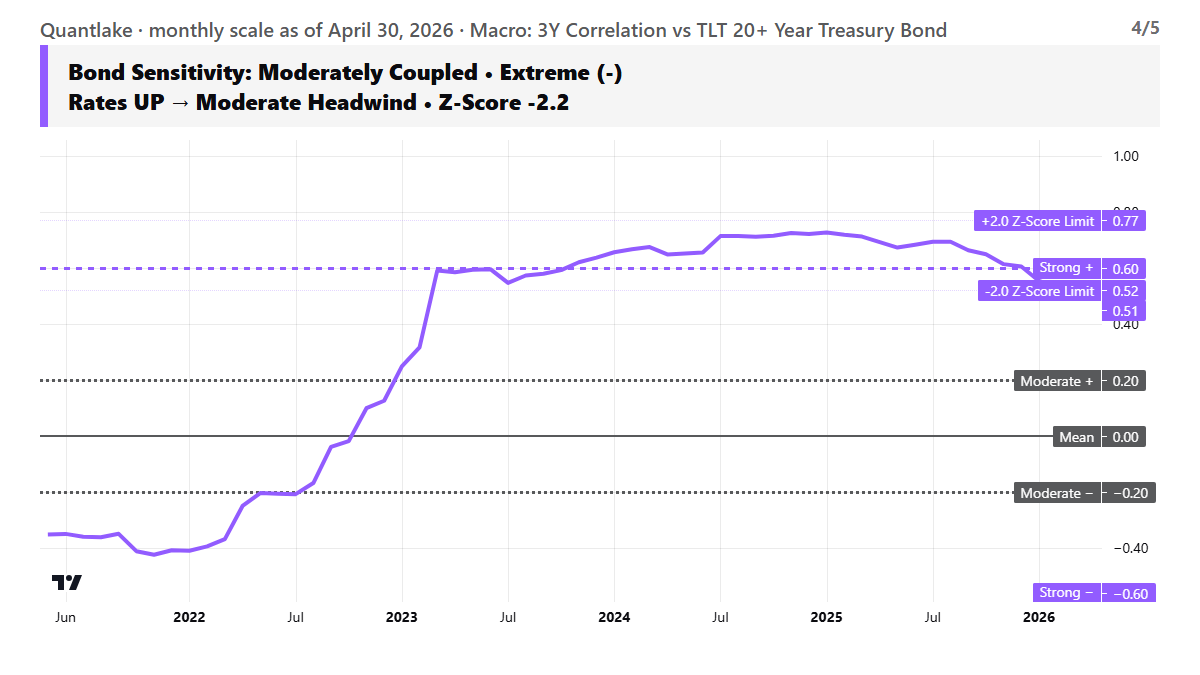

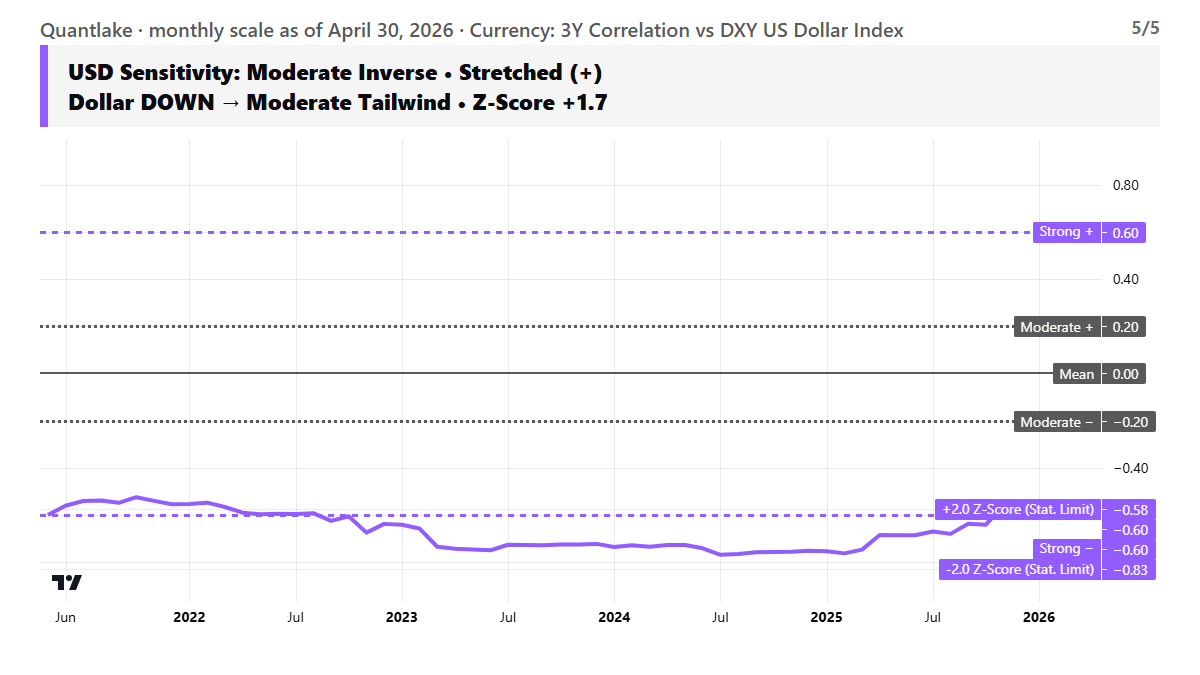

Rates and the dollar are helping, but neither signal is clean enough to carry the setup alone. Bond correlation is 0.51, down from 0.55 three months ago, and bond-sensitivity Z-score is -2.2, showing current rate linkage is unusually low relative to its own history. That matters in a market where the Federal Reserve held rates at 3.50% to 3.75% on April 29 and flagged inflation pressure from higher energy prices. At the same time, DXY (U.S. Dollar Index) correlation is -0.60 versus -0.61 three months ago, so the fund would still benefit if the dollar eases, but that tailwind is stable rather than strengthening. China adds the same two-sided message: late-April manufacturing stayed in expansion and export orders improved, while domestic demand stayed soft and services contracted.

A regime change would need more than a pause in momentum. It would likely take relative strength falling below its long-term average, together with bond correlation turning back up from 0.51 and dollar sensitivity becoming more negative than -0.60. That would leave the fund more exposed to rising yields and a firmer U.S. dollar at the same time.

Glossary

10-month moving average (SMA): A trend line that averages the last 10 months of closing prices. Price above it signals an uptrend; below signals a downtrend.

Beta: How much an ETF moves relative to the S&P 500. Below 1 = less volatile than the market; above 1 = more volatile.

Sortino ratio: A risk-adjusted return measure that only penalises downside volatility (losses), not general price swings. Higher is better; above 1.0 is solid.

Z-score: How far a value sits from its 3-year average, in units of standard deviation. Beyond +/-2 is statistically unusual and tends to mean-revert.

Correlation: A value from -1 to +1 measuring how two assets move together. +1 = lockstep; -1 = opposite directions; 0 = no relationship.

For informational purposes only; not financial advice.

Romain Gandon — CEO, Quantlake